The NICU Specialist Built to Last But Priced Like It’s Dead

After divesting non-core units, cutting debt, and stabilizing physician turnover, Pediatrix is back to doing one thing well. Hospital-based newborn and maternal care. The market still hasn’t noticed.

👋 Hello all

Welcome to 📉 DeepValue Capital 📈

It’s Friday which means First Look time. These are early-stage ideas, still under review that are interesting enough I wanted to share them here.

This week’s setup?

A hospital-based turnaround that just raised guidance and trades at 5.2x normalized cash flow.

Before we dive in, here’s how my portfolio has performed:

📈 From Jan 1, 2024 to April 30 2025, my personal portfolio is up 129.23%. Then YTD after an incredible May, +55%.

All from setups like this, mispriced and misunderstood.

Want setups like this before the market sees them? Hit subscribe below to get them right in your inbox.

This week’s First Look: Pediatrix Medical Group (MD)

Wall Street sees an old healthcare roll-up. But this company has gotten leaner and still trades like it’s dead. Even after a solid quarter where margins expanded and the company raised guidance.

This post covers:

✅ What Pediatrix actually does

✅ Why this turnaround may stick

✅ Key risks + back-of-the-napkin valuation

✅ What They Actually Do

Pediatrix runs a network of specialized doctors who work in hospitals.

Their doctors care for:

Premature babies in NICUs

High-risk pregnancies through maternal-fetal medicine

Critically ill kids through pediatric intensivists

And OB hospitalists (doctors who deliver babies but don’t run a private office)

They don’t own hospitals. They contract with hospitals who need help staffing these high-skill roles 24/7.

Hospitals often struggle to recruit and manage specialized physicians like neonatologists or OB hospitalists, especially in smaller or rural facilities.

That’s where Pediatrix comes in.

The company partners directly with hospitals to provide full staffing for these roles. Handling everything from hiring and scheduling to payroll, billing, and collections. In return, hospitals either pay Pediatrix directly or coordinate with insurance (including Medicaid) to reimburse the services.

For hospitals, it’s a faster, more cost-effective alternative to building in-house teams. For Pediatrix, it creates steady, contract-based revenue that’s tied to hospital demand.

🔥 Why It’s Interesting

MD has cut aggressively to focus their core.

Since 2020, Pediatrix has divested nearly every non-core unit:

2020: Sold its anesthesiology division

2021: Sold its radiology group (vRad)

2024: Exited all affiliate-based offices, including most outpatient practices, retaining only maternal-fetal groups

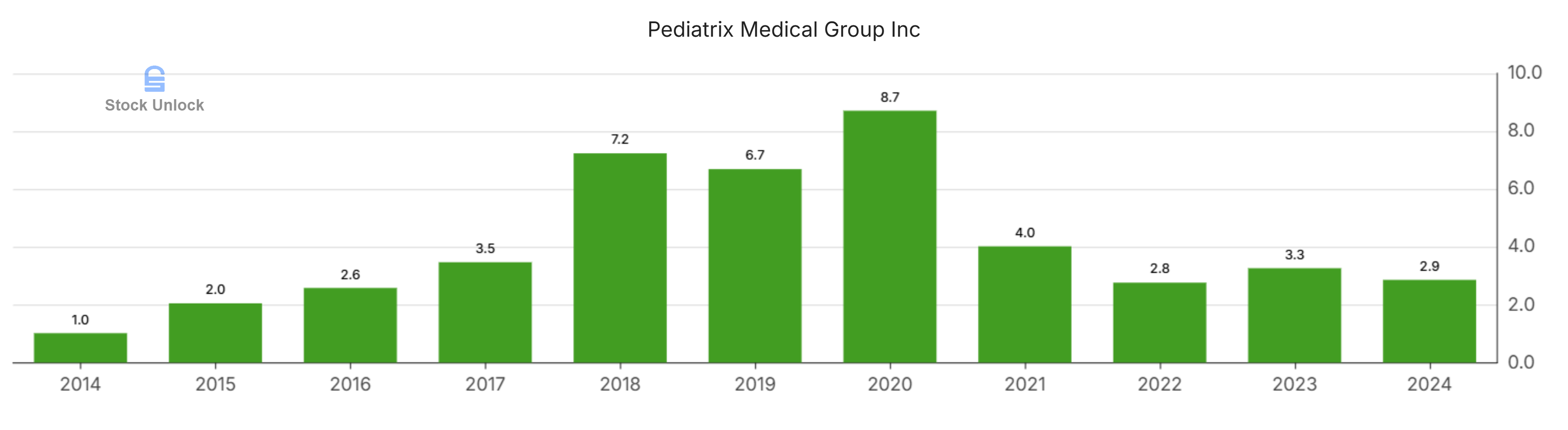

It used divestiture proceeds to cut debt nearly in half, and now operates with debt to EBITDA of 2.72x in the TTM. Down from 8.7x in 2020. That gives it breathing room.

These weren’t small exits. The most recent divestiture alone accounted for $200M in annual revenue, but it was low-margin and distracting. With these businesses off the books, Pediatrix is now centered solely on its hospital-based core. The impact is already showing up. Net margin jumped from 0.8% to 4.5% year-over-year.

Labor pressure is finally easing.

After a rough stretch during COVID and the Great Resignation, physician turnover is down. Salary growth has now decelerated four quarters in a row, and leadership is focused on retention and recruitment. A must in this high-skill, high-touch model.

It’s always been a high-quality business.

Even at the lowest point of this downturn, Pediatrix stayed cash-flow positive. That alone sets it apart from most broken healthcare roll-ups.

But the deeper story is return on capital.

Since 2000, Pediatrix’s median return on capital employed (ROCE) has been over 15%. A clear marker of a business that knows how to reinvest effectively. Despite recent turbulence, its trailing 12-month ROCE just hit 11.5%, and will continue to climb.

This isn’t a capital-light software company. It’s a labor-heavy operator that still puts up double-digit returns in rough environments.

Macro tailwinds are building.

The U.S. is facing a shortage of OB-GYNs, with the American Congress of Obstetricians and Gynecologists projecting steep declines in workforce supply over the next 20 years.

At the same time, more women are delaying childbirth. Which increases the rate of high-risk pregnancies and drives sustained demand for neonatal and maternal-fetal care.

Hospitals are responding by outsourcing more. The hospital outsourcing market is projected to grow from $382B in 2024 to over $1T by 2034, a 10.3% CAGR. Staffing hard-to-fill specialties like neonatology and OB hospitalists through partners like Pediatrix is becoming the norm, not the exception.

Meanwhile, birth rates in the South remain relatively stable. Texas ranks near the top nationally, with a birth rate of 13.2 per 1,000. And Florida also remains above the national average.

That matters because Pediatrix is deeply entrenched in these regions. And structurally, there are more tailwind coming. Millennials are the largest generation in U.S. history, and they're entering peak family formation years.

As that cohort begins to have children over the next 5–10 years, we could see a modest rebound in birth trends. Especially in growth regions like the Southeast where Pediatrix already dominates.

None of these shifts move the stock on their own. But together, they support the idea that margin recovery isn’t a fluke, it’s supported by structural tailwinds.

⚠️ What I’m Still Figuring Out

These are the questions I’d need answered before this becomes a position:

Are management incentives aligned with shareholders?

How does MD compare to peers and competitors?

Their CEO is a turnaround specialist but what is his track record and style? How can this be expected to play out?

Those above are important but the following two are risks that MUST be understood.

Can they reduce exposure to Medicaid over time?

Will labor pressure stay under control?

Right now, early signs are encouraging but there is still a lot to understand before I would have full confidence.

📉 Back-of-the-Napkin Valuation

Let’s run a base case:

2025 revenue: $1.9B

Grow at 6% annually → 2028 revenue: $2.26B

Apply 12% normalized FCF margin → FCF = ~$271M

Put a 13x FCF multiple on that →$3.52B market cap by 2028

Today’s market cap = $1.18B

That’s a 3x in 3.5 years, or ~37% CAGR

MD is a very interesting setup in healthcare, a sector I have really been diving into. There are still questions I have but this one was worth sharing.

What do you think of the company?

📬 4 More Articles You’ll Love

New here? Start with these:

Read This Before You Subscribe.... After Works Fine Too - Who I am and what DeepValue Capital Offers.

My Step-by-Step Guide to Outperformance - My investing system broken down in step by step detail for you.

Disclaimer:

This content is provided for informational and entertainment purposes only and should not be construed as professional financial or investment advice. The opinions expressed herein are solely those of the author, based on personal research and analysis, and do not reflect the views or advice of any financial institutions or licensed professionals. I do not have access to your personal financial situation, goals, risk tolerance, or investment preferences, and therefore cannot provide personalized investment recommendations. It is essential that you conduct your own research, carefully consider all relevant factors, and consult with a licensed financial advisor or other professional before making any investment decisions. Investing inherently involves risk, including the potential loss of principal, and past performance is not indicative of future results. I am not responsible for any decisions, actions, or outcomes resulting from the use of this content. Always ensure that your investments align with your personal financial situation and long-term objectives.

Did you Buy the dip?