Buried in Fear this $1B Giant is Waking

Despite FX drag and market fear, IHS is building margin, selling non-core assets, and hiding real upside.

👋 Hello all

Welcome to 📉 DeepValue Capital 📈

Every week on Wednesday I send out a Portfolio Spotlight covering a position I hold with all the important news. Then at the end I lay bare all my portfolio, positions, weights, and NEW this week my target share prices.

This week I cover a company that reported earnings on May 20th.

Their free cash flow margins are climbing

They sold a non-core business at 5x their current multiple

And management is clearly sandbagging their 2025 outlook

From what I see, there’s still 6.5x upside from here.

But before we dive in, let’s cover how my portfolio has performed.

From January 1st, 2024 to April 30th, 2025 I'm up 129.23%, and after a fantastic May, up 53.6% year to date.

If you want real updates like this before the market figures it out subscribe below.

I share the full breakdowns, valuation math, and trade alerts behind a portfolio that is CRUSHING the market.

I can’t promise I will never make a mistake but I can promise I will be putting my money where my mouth is, constantly learn, and be upfront with you.

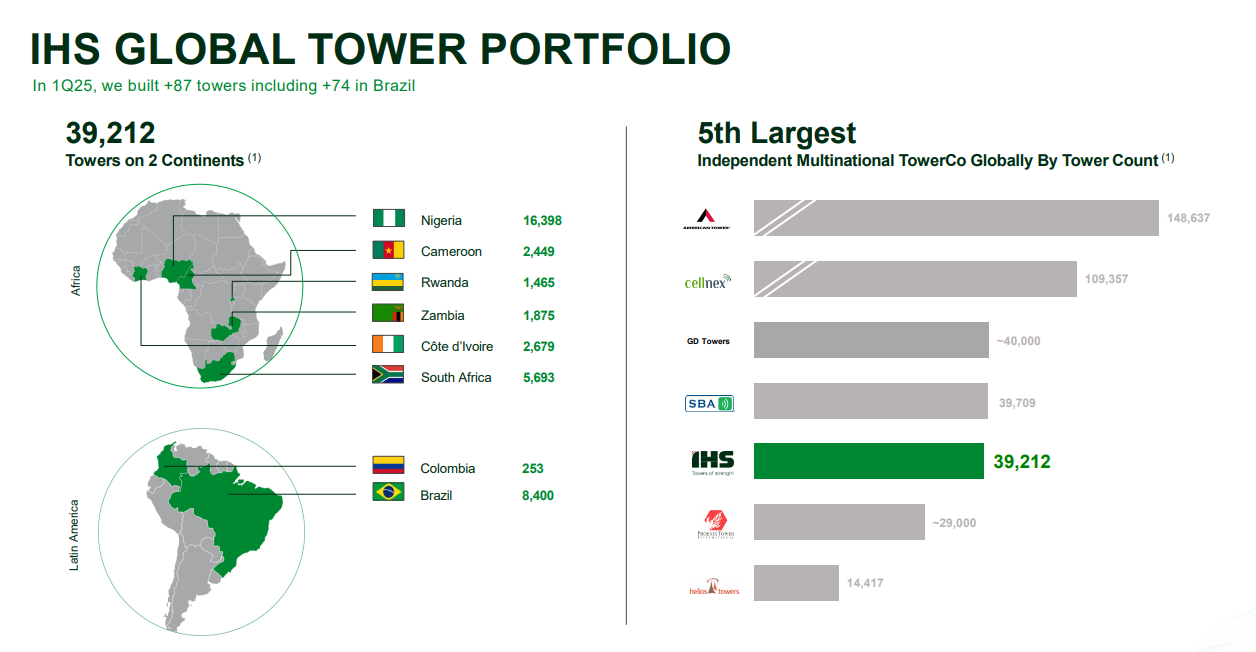

This Week’s Spotlight: IHS Holdings (IHS)

The market sees an FX-exposed telecom name stuck in Nigeria. I see a high-margin infrastructure compounder with a $1B in run-rate FCF by 2029.

Let’s break it down:

✅ What they actually do

✅ What is changing

✅ Math behind the 6.5x setup from today’s levels

What does IHS do?

IHS Holdings builds and operates telecom towers in fast-growing markets. Mainly Nigeria, Brazil, and other regions where mobile data is still scaling fast.

Think of a tower being rented out like an apartment building. Each mobile carrier (MTN, Airtel, etc.) pays to hang their antennas on the structure.

These are long-term, inflation-linked contracts typically 5 to 10+ years.

Adding a new tenant? Almost pure profit. Same tower, more rent.

It’s a classic infrastructure-margin model:

Recurring cash flows

Predictable CPI escalations

Minimal incremental cost per new tenant

And the tailwinds here are massive.

Data usage in IHS markets is expected to grow at 21.2% CAGR through 2029. 4G/5G penetration is projected to rise from 57% in 2024 to 86% by 2029.

That means more users, more bandwidth demand, and more reasons for carriers to lease additional tower space.

Q1 Earnings Highlights

Here’s what stood out from Q1:

Keep reading with a 7-day free trial

Subscribe to DeepValue Capital to keep reading this post and get 7 days of free access to the full post archives.