New Idea ($ELD) | The 185 Years Young Farm Supplier with 3x Upside

An early-stage breakdown of Elders (ASX: ELD). A high-trust Australian ag business with optionality if the cycle keeps turning.

👋 Hey All

Welcome to 📉 DeepValue Capital 📈

The Turnaround Investment Newsletter

Every Friday, I share one early-stage idea most investors are ignoring. Not a buy call, just a head start. I do the digging so you don’t have to.

This week’s idea?

A 185-year-old ag supplier with a shot at a 3x if the cycle turns. They are the #2 player in the Australian market where trust is everything. Good thing they have had some time to build relationships!

Before we dive in, here’s why you should listen to me:

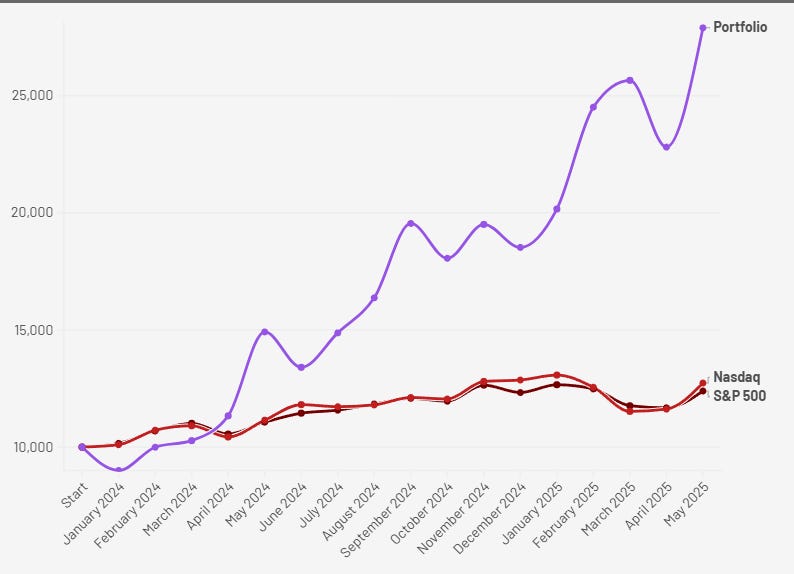

📈 From Jan 2024 to May 2025, my portfolio is up 178.98%. That’s 85.23% in 2024 and another 50.61% so far in 2025 through May.

Still not sure? On 8/10/24, I covered a little-known name: IHS. It’s up 107% since.

I am not promising perfection or that I won’t make mistakes. But that I will put my money where my mouth is, work to get you the best information, and keep getting better.

Want the next deep dive, company update, and early setup before the market catches on?

Start your 14-day free trial and get full access to my portfolio, trade alerts, and turnaround research.

If you’ve got $20K (Or more) invested, a 5% edge is worth at least $1,000.

DeepValue Capital costs $209/year and that upside compounds.

👇 Try it free. Cancel anytime.

This Week’s First Look: Elders (ASX: ELD)

This company is a one-stop shop for Australian farmers. From seeds and fertilizers to cattle auctions and farm loans. After two brutal years of drought and falling prices, the ag cycle finally looks like it might be turning.

Let’s see what happens when a high-trust operator gets a tailwind again.

This post covers:

✅ What Elders actually does

✅ What’s quietly shifting in their favor

✅ What I’m still figuring out

✅ Upside math if the rebound sticks

🧠 What the Company Actually Does

Elders is a 185-year-old Australian company that acts as the glue of the country’s farming economy. They don’t own the land or the livestock. Instead, they sell the tools, services, and advice that make farming work.

If you're a farmer in Australia, there’s a good chance you rely on Elders for one or all of the following:

🛒 Rural Products (~55–60% of revenue):

Elders sells core farm inputs, seed, chemicals, fencing, tools, through a national retail footprint. This is high-volume, lower-margin business that grows when grain prices are strong or rainfall is good.🐄 Agency Services (~35–40%):

This is Elders’ broker arm. They help farmers transact: livestock, wool, and feedlot services. They take a cut of each transaction meaning they don’t need to carry inventory or take price risk. Revenue here is tied directly to volume and price movement.🏡 Financial & Real Estate (~5%):

The smallest segment, but high margin. Elders brokers farm properties, sells rural insurance, and offers agrifinance (like livestock loans and seasonal funding). These services are sticky they make clients less likely to leave for a competitor.

Revenue is recurring (farmers need inputs every season). But volatile, because weather, prices, and confidence all swing year to year.

It’s a razor-thin, high-trust business. Good thing Elders has been around for 185 years to build that trust.

🔥 Why It’s Interesting

Elders is coming off a brutal two-year stretch. Drought conditions, falling livestock prices, an weaker farmer sentiment crushed earnings. Net income dropped from $163M in 2022 to just $45M in 2024.

But that pain is setting the stage for a potential cyclical snapback.

Here’s what’s changing now:

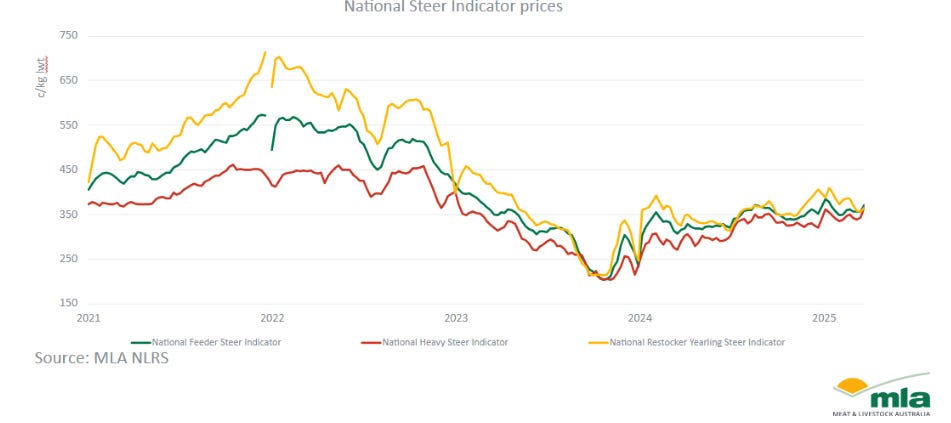

Cattle Prices Are Rising Again

Slaughter cattle prices are up 20–30¢/kg live weight since late 2024. Heavy steers are now at 355¢/kg up from below 250¢ in late 2023. That flows directly into Elders’ livestock commission revenue, its most sensitive profit driver.

Processing and Export Are Rebounding

Local processors have ramped weekly capacity from 130K to 155K head. Live export permits are back on schedule. Vietnam and Indonesia are placing new orders. More throughput = more agency revenue.

Winter Crop Setup Looks Solid

About 60% of winter crops are planted under good to excellent conditions. While some regions remain patchy, late April rains helped boost confidence. Strong plantings → stronger demand for fertilizer, seed, and chemicals → higher merchandise revenue.

Global Tailwinds Are Taking Shape

U.S. beef supply is falling and lean beef prices are spiking in export markets. Meanwhile, Ukraine’s wheat harvest is forecast at a 13-year low. All of this improves export pricing for Australian ag and indirectly benefits Elders.

⚠ What I’m Still Figuring Out

The cycle look like it might finally be turning but there are still a few things I need to get clearer on:

How do different catalysts actually flow through the P&L?

I understand that rising cattle prices and restocking activity are both good, but which matters more? How do timing and sequence affect revenue? I want to dig deeper into how specific market shifts (like slaughter margins vs. restocker demand) actually move commissions and merchandise sales.

Will global supply problems turn into real pricing power?

Australia’s winter crop is off to a strong start. Ukraine’s harvest could hit a 13-year low. But will that actually lift grain prices? Until pricing rebounds, input demand could stay muted.

What are management incentives tied to?

CEO Mark Allison has been in the seat since 2014. Revenue has more than doubled, but earnings have dropped sharply. I haven’t dug in to understand comp targets, insider ownership, or what management is really optimizing for.

How exposed is this business to weather over the next 2–3 years?

Obviously agriculture is cyclical, but I want to better understand just how leveraged Elders is to rainfall patterns and what the long-range weather expectations look like in core farming regions. If El Niño sticks around or climate variability worsens, does the downside get uglier than I think?

Elders is a complex business. It doesn’t move on just one lever. It’s a blend of local weather, global commodity prices, farmer psychology, and policy. You need to understand that very clearly before buying a company like this.

This post isn’t a full thesis, it’s just a first look. If I get a clearer read on how different catalysts translates into earnings, it might move higher on the watchlist.

📉 Back-of-the-Napkin Valuation

Let’s assume the cycle turns in Elders’ favor with key catalysts falling into place. Here’s what that could look like:

2024 Revenue: A$3.13B

Target Growth: +20% by FY2029 → A$3.76B

Estimated FCF Margin: 6.5% (similar to peak level seen in 2020)

Free Cash Flow: A$3.76B × 6.5% = A$244M

Now apply a 14x P/FCF multiple, consistent with the 2020 margin peak:

Implied Valuation: A$244M × 14 = A$3.42B

At today’s market cap of A$1.14B, that’s 3x upside or roughly a 37% annualized CAGR over 3.5 years assuming no change in share count. Not bad at all for an almost 200 year old business!

There is obviously still a lot of work to be done but this one was interesting enough I wanted to share it!

If you’ve got thoughts on Elders, I’d love to hear them. Always open to pushback, data I missed, or ideas you think deserve a closer look.

📬 4 More Articles You’ll Love

New here? Start with these:

Read This Before You Subscribe.... After Works Fine Too - Who I am and what DeepValue Capital Offers.

My Step-by-Step Guide to Outperformance - My investing system broken down in step by step detail for you.

Disclaimer:

This content is provided for informational and entertainment purposes only and should not be construed as professional financial or investment advice. The opinions expressed herein are solely those of the author, based on personal research and analysis, and do not reflect the views or advice of any financial institutions or licensed professionals. I do not have access to your personal financial situation, goals, risk tolerance, or investment preferences, and therefore cannot provide personalized investment recommendations. It is essential that you conduct your own research, carefully consider all relevant factors, and consult with a licensed financial advisor or other professional before making any investment decisions. Investing inherently involves risk, including the potential loss of principal, and past performance is not indicative of future results. I am not responsible for any decisions, actions, or outcomes resulting from the use of this content. Always ensure that your investments align with your personal financial situation and long-term objectives.

Excellent write up do u have Direct message or can I email you directly thanks Keith