Portfolio Spotlight ($CRK) | The Lowest Cost Producer Profiting from the AI Power Crisis

Breaking down the lowest cost natural gas producer in the country, how it is riding two massive tailwinds, and what the they are worth.

👋 Hello all!

Welcome to 📉 DeepValue Capital 📈

THE Turnaround Investing Newsletter

Every Wednesday, I break down a stock I own. You get the full thesis, what’s changed, and the conviction to hold through the noise. You can’t get the full benefit if you sell too early, so don’t.

This week’s spotlight? The lowest-cost gas driller in America positioned to feed the fastest electricity demand growth in 30 years, driven by LNG and data centers.

Before we dive in, here’s why you should listen to me:

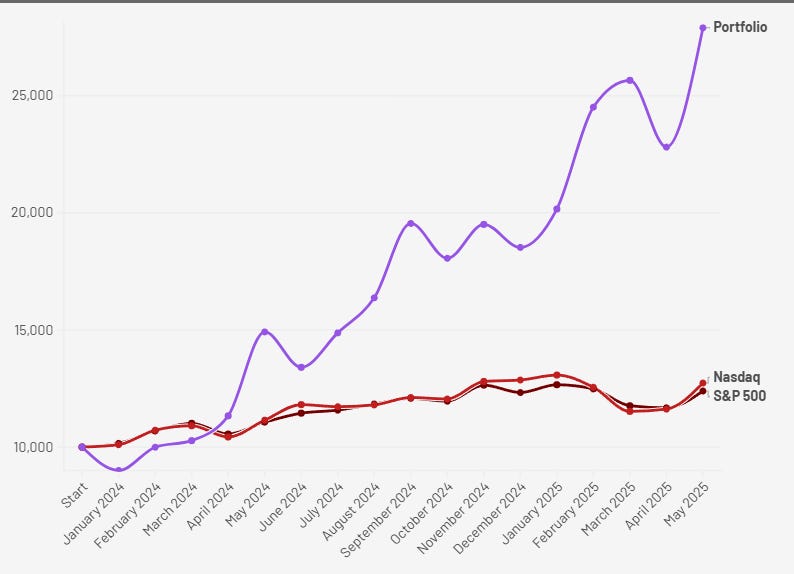

📈 From Jan 2024 to May 2025, my portfolio is up 178.98%. That’s 85.23% in 2024 and another 50.61% so far in 2025.

Still not sure? On 8/10/24, I covered a little-known name: IHS. It’s up 107% since.

I am not promising perfection or that I won’t make mistakes. But that I will put my money where my mouth is, work to get you the best information, and keep getting better.

Want the next deep dive, company update, and early setup before the market catches on?

Start your 14-day free trial and get full access to my portfolio, trade alerts, and turnaround research.

If you’ve got $20K (Or more) invested, a 5% edge is worth at least $1,000.

DeepValue Capital costs $209/year and that edge compounds..

👇 Try it free. Cancel anytime.

🔦 This Week’s Portfolio Spotlight: Comstock Resources (CRK)

No one’s talking about natural gas, but it’s quietly becoming the most important fuel in the world. Comstock is the lowest-cost gas producer in America. Perfectly positioned to ride a once-in-a-generation demand surge, from data centers, LNG exports, and power-hungry infrastructure.

My thesis: Comstock stays disciplined, expands reserves, and gets revalued as gas prices rise and demand compounds into 2027.

Valuation upside: ~100% upside or 31% CAGR through 2027, even after the stock’s huge run.

Here’s what’s coming:

✅ What Comstock actually does and how it wins

✅ The full supply/demand setup

✅ My valuation

And after a full breakdown of my portfolio, my holdings, costs basis, weights, and targets.

🧠 What the Company Actually Does

Comstock Resources is a pure-play natural gas producer based in Frisco, Texas. They don’t own pipelines, refineries, or transport assets. They drill gas wells. That’s it.

Nearly all of their revenue comes from natural gas, with just a small contribution from oil sales.

Their business is straightforward:

Acquire acreage

Drill horizontally into high-pressure rock

Extract gas at low cost

Sell into nearby infrastructure

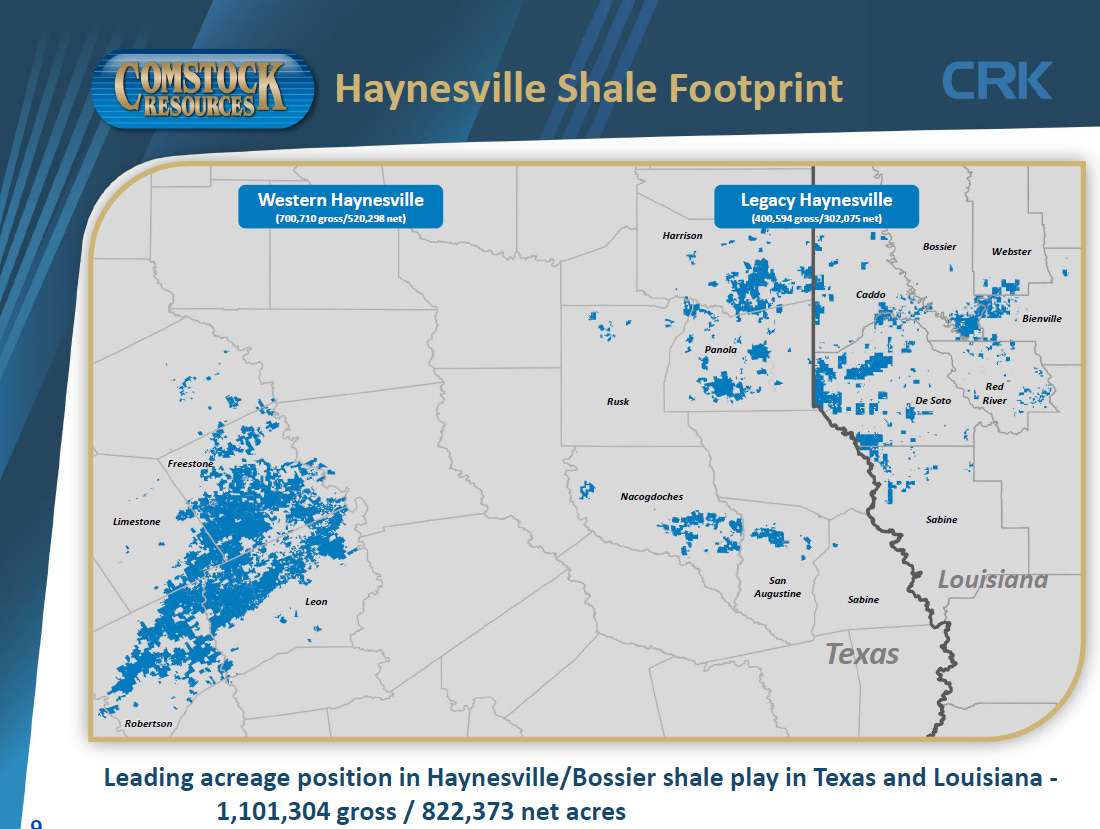

As of Q1 2025, Comstock controls:

That makes them one of the largest operators in the Haynesville. A high-output shale basin in North Louisiana and East Texas known for its rich gas deposits and close proximity to pipelines and LNG3 terminals along the Gulf Coast.

Comstock’s recent focus has been expanding westward into a less-developed zone called Western Haynesville. Here wells are deeper, more expensive to drill, but also significantly more productive.

This isn't a spray-and-pray E&P company. It’s a precision, gas-only machine built around one idea:

Be the lowest-cost, high-volume dry gas4 producer in one of the most infrastructure-rich basins in the U.S.

Jay Allison has led that mission since 1988. Through booms, busts, and shale revolutions, he’s stayed focused on one commodity and one basin. And it shows.

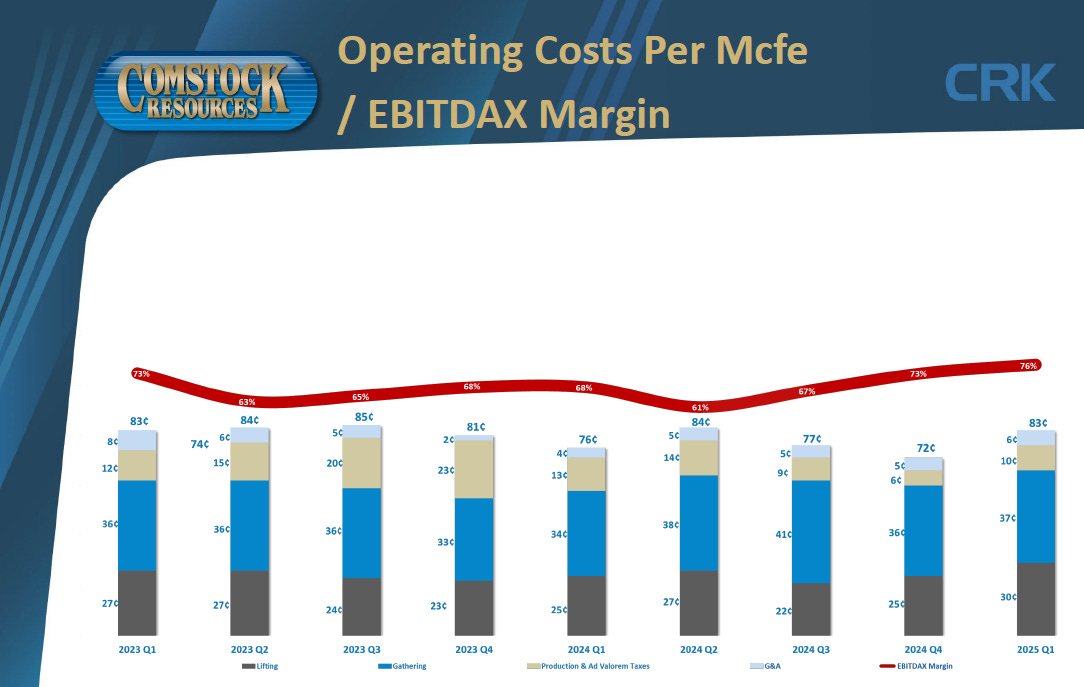

When you’re selling a commodity like gas, every penny of cost matters.

Comstock’s ability to consistently operate at the lowest cost in the industry is more than just a margin booster, it’s a competitive weapon.

Lower costs mean:

They stay profitable at lower gas prices.

They can outlast higher-cost peers in downturns.

And they don’t need to hedge as aggressively to protect cash flow.

When prices fall, Comstock takes share. When prices rise, it mints cash. That’s the setup.

🧠 The Thesis

Natural gas bottomed around $1.50 in February 2024. Since then it’s rallied ~140%, trading around $3.60 today

That short-term pop is only the start. Here’s what's fueling the case:

Keep reading with a 7-day free trial

Subscribe to DeepValue Capital to keep reading this post and get 7 days of free access to the full post archives.