KBR Inc (KBR) Notes

Welcome to 📉DeepValue Capital📈

I’m Kyler Johnson, a husband, dad, and self taught investor of 7 years.

23K+ subscribers and 271.16% returns from Jan 2024 to May 2026. I buy turnarounds and good companies at great prices.

KBR has supported NASA since the 1960s, licenses the technology behind half the world's ammonia, and holds one of three prime spots on the Army's $82 billion overseas logistics program.

Defense spending is set to pass $1 trillion for the first time in FY26, ammonia is heading into a build cycle, and yet the stock is down almost 50% from its high.

On top of that, the company is splitting itself into two separate public companies to remove the conglomerate discount.

Ticker: KBR 0.00%↑

Market Cap: ~$3.5B

TTM Revenue: $7.7B

TTM FCF: $489M

EV/FCF: 13.75x

5yr Median ROIC: 11.31%

The Company

KBR is two businesses sharing one ticker, but that is going to change.

On September 24, 2025, the board approved a plan to spin off Mission Technology Solutions (MTS) as a standalone public company in the second half of 2026, leaving Sustainable Technology Solutions (STS) as the company that remains.

MTS

MTS sells the time and expertise of cleared engineers, scientists, and logistics specialists to militaries and government agencies, mostly the U.S. Department of Defense and NASA.

It accounts for about 72% of consolidated revenue. The work spans high-end systems engineering on classified national security programs, operational support for NASA’s human spaceflight, and overseas base operations for U.S. and allied forces. It also includes critical infrastructure engineering for governments, covering things like water, transportation, energy, and power.

Contracts run five to ten years with options to extend, and renewals are the norm. Replacing the incumbent means clearing a new workforce from scratch, which takes years, so the work tends to stay put.

Operating margins are the lower of the two segments at 8.3% in 2025, but the relationships run deep. Brown & Root has been embedded at NASA continuously since the 1960s, and KBR is one of only three primary contractors on LOGCAP V, the Army’s $82 billion overseas military logistics program. Those are not positions a rival wins by underbidding.

STS

STS, the other 28% of consolidated revenue, is a very different business, with operating margins of 21.6% in 2025, more than double MTS. It combines process technology licensing, engineering services billed by the hour, and equity earnings from joint ventures like its 45% interest in a major LNG project.

The licensing is where STS really shines, especially in ammonia, with 50% of global licensed capacity, and refining residue, where they hold 90% market share. The list of licensors that can write performance guarantees on multi-billion-dollar plants is short, and getting on it takes decades of operating history. Insurance underwriters won’t write policies on these plants without a licensor standing behind them, and lenders won’t finance them.1

Once a process is licensed, KBR earns recurring revenue from catalyst replacements every five to ten years across hundreds of plants, often for decades.

Why They’re Interesting

Several long-term trends are moving in KBR's favor at once.

Defense Spending

The FY27 defense budget request calls for $1.5 trillion, the largest in U.S. history, building on the first-ever $1 trillion defense budget in FY26. The new money flows disproportionately into research and development, integrated air and missile defense, space, hypersonics, and autonomous systems. That is exactly what MTS sells, and it will pull margins up over time.

Allied spending adds to it, with NATO targeting 5% of GDP by 2035.2

Ammonia

Global ammonia capacity is set to grow about 21% to 290 million tonnes by 20303, and 84% of that new capacity is conventional or carbon-captured ammonia, where KBR is strongest. The other 16% is near-zero-emission.

Near-zero-emission is the part that gets the headlines, but it is the smaller story. The announced low-emission pipeline looks enormous, more than 300 million tonnes, 125% of today's entire global capacity.4 Most of those projects will never reach a final investment decision, so the capacity that actually gets built still skews conventional, but that pipeline highlights how massive demand is.

KBR’s PURIFIER process uses 12 to 15% less natural gas than competing oxygen-based designs, and its Ammonia 10,000 technology triples single-train capacity to 10,000 metric tons per day, which no competitor offers.

Since 1943, KBR has licensed, engineered, or constructed more than 250 ammonia plants worldwide.

Civil Nuclear

Western civil nuclear is in its first growth cycle since the 1980s, with the U.S., UK, Europe, and Canada all targeting major capacity increases through 2050.5

KBR's strength here is concentrated in the UK, where it has grown its nuclear team about 370% since 2020 to over 1,000 professionals and holds positions on Sizewell C, the Rolls-Royce SMR program, and Sellafield decommissioning.

The OpEx Pivot

In January 2026, KBR’s industrial maintenance joint venture, Brown & Root Industrial Services, closed a $115 million acquisition of SWAT, short for Specialty Welding and Turnarounds. The deal more than doubled the joint venture’s EBITDA, and KBR holds a significant stake in it.

The work is recurring industrial maintenance at refineries, chemical plants, and other heavy-process facilities. It is contracted and tied to plant operations rather than new construction, which makes the revenue more predictable than the rest of STS. Management has been explicit about wanting more of this kind of work, organically and through further deals.

Energy Security

The closure of the Strait of Hormuz during the Iran war showed how dependent the world still is on Middle East energy. Wood Mackenzie called a prolonged closure “the single greatest threat to global energy markets in decades.”

Wood Mackenzie’s view is that even after the strait reopens, the episode pushes import-dependent countries to strengthen their own energy security and lean less on the region. That means building and hardening energy infrastructure, which is engineering work. KBR does it for governments through MTS and for private operators through STS.

There is also the damaged infrastructure itself, which needs repair and reinforcement. A direct KBR peer shows the demand is already real. McDermott International has continued Gulf energy work right through the conflict, with clients like Saudi Aramco and ADNOC pressing to speed up projects already underway, and it guided its 2026 earnings about 21% higher.

The Spin-Off

Most of the catalysts above play out over years. The spin-off is the near term specific corporate action with a date attached, and it targets a discount that already exists.

Conglomerates that combine very different businesses trade at a discount to the sum of their parts, and that is especially true for one as complex as KBR. The company gets priced by whichever investor group is willing to tolerate both halves, which is rarely the group willing to pay a full price for either.

Academic research on U.S. spin-offs finds the parent and the spun-off company, taken together, tend to outperform the market for the first two to three years after separation. In one study, the newly spun-off businesses outperformed by about 8% in their first year alone.6 The discount is real, and the mechanism for closing it is now in motion.

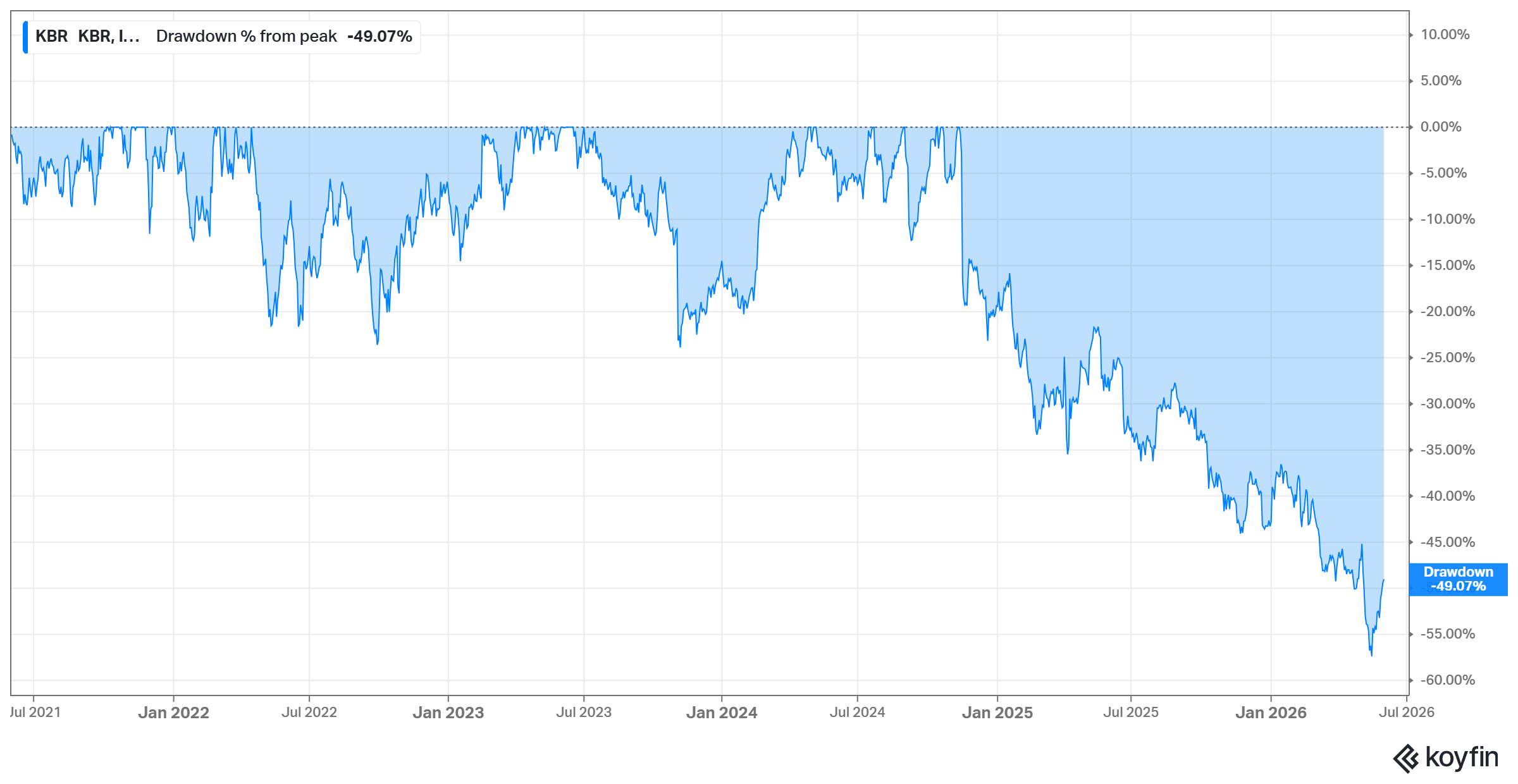

The Drawdown

As of today KBR trades around $36 per share, down almost 50% from its late-2024 peak near $73.

The market sold it off for real reasons, which I will get to. But a good business with several long-term tailwinds lining up at once, in a drawdown this size, caught my attention.

Forward Returns

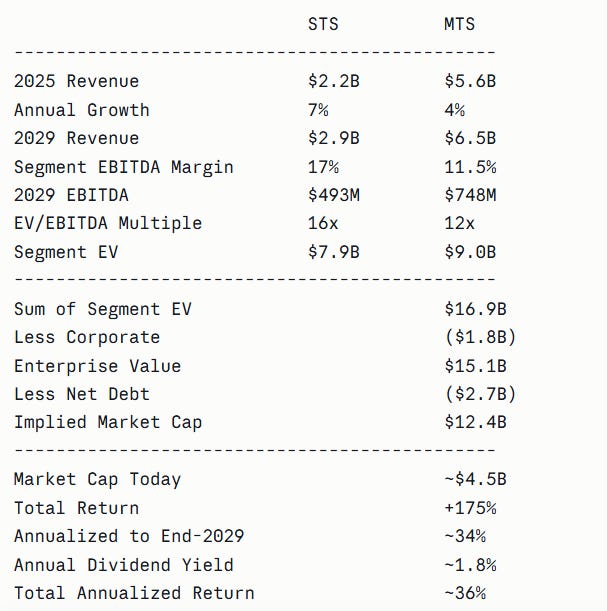

I kept STS and MTS growth at 7% and 4% as a conservative base well below managements guidance due to the uncertainty of awards inherent in their businesses.

On margin. The base business does improve as other joint ventures contribute and the contract mix moves up-market, but I do not think they fully replace Plaquemines LNG. That is why my 2029 consolidated EBITDA margin lands near 11.8%, below the 12.8% management targets for 2027. The honest read is steady expansion in the base business, hidden by LNG fading out.7

For net debt, I assume it grows roughly in line with revenue., from about $2.2 billion today to about $2.7 billion. That just assumes they hold leverage about steady as they get bigger.

I also hold share count flat over the period, so the move in market cap is the move per share. KBR has been buying back stock, so if anything that understates the per-share result.

The multiples are where the two businesses part ways. STS should trade at a premium. Its closest public comparable is Worley, which does some of the same engineering work, but STS also owns a portfolio of licensed process technologies that throw off recurring, high-margin revenue Worley does not have. 16x EV/EBITDA is reasonable for that.8

MTS is a government services business, in the company of Leidos, CACI, and Booz Allen at roughly 12 to 15x. Given its slower growth and a couple of recent contract stumbles, I anchor to the low end at 12x.9

Forward returns clear my hurdle comfortably, but they are not guaranteed by any means.

As we get closer to the spin, we should get a lot more detail on how each business looks standalone, including the capital structure each one carries. For now, this is my framework for what they are worth a few years out.

Why I’m on the Sidelines

I do not own KBR. Everything below is what has kept me from taking a swing so far.

The HomeSafe Cancellation

HomeSafe was a 72%-owned KBR joint venture that won a $20 billion contract from U.S. Transportation Command (TRANSCOM) in November 2021 to consolidate the U.S. military’s household goods relocation under a single primary contractor.

TRANSCOM terminated it for cause on June 18, 2025. The financial impact was modest, but the credibility impact was real.

On the May 6th Q1 earnings call, CEO Stuart Bradie called the TRANSCOM relationship “excellent” and said he was “very confident in the future of this program.” Forty-three days later, TRANSCOM terminated for cause.

A CEO calling a customer relationship excellent weeks before that customer terminates for cause is a different category than a forecast that does not pan out. Bradie’s 2014 to 2024 track record earns him the benefit of the doubt10, but not blind trust.

The Margin Cliff

KBR holds 45% of the KZJV joint venture executing the Plaquemines LNG project for Venture Global. Its share of that JV’s profit comes through as equity earnings, which is what pushed STS adjusted EBITDA margins to 23.5% in Q3 2025. That contribution rolls off through 2026 and into early 2027.

Lake Charles was supposed to follow it. KBR and Technip Energies held the engineering and construction contract there, set up to run through a joint venture the same way Plaquemines does. But in December 2025 Energy Transfer suspended the project to put its capital into pipelines instead, leaving it open to a third-party developer. The other LNG work KBR has in flight is mostly consolidated fee-for-service, revenue but at much lower margins.

Management’s 2026 STS guidance is still 20%+, because Plaquemines is still contributing this year. The real question is what STS looks like once it is gone. On the most recent earnings call, management gave a clear answer: without the LNG contribution, margins run around 15%.

The step down is a margin problem, not a volume one. STS backlog grew more than 20% excluding Plaquemines, but the work filling it pays far less than the equity earnings rolling off. So the business has to be valued on steady-state margins. They likely drift up from 15% as the OpEx and technology mix grows, but a return to 20%+ is very unlikely without another major equity-participation project.

Iran War Timing

Management has been clear that work in the region is continuing despite the conflict. The risk is on new projects. If it drags on, I would expect some regional work starts to slip, though when and for how long is hard to know.

Forced Selling Post-Spin

Spin-offs reliably create forced selling. Funds and institutions that cannot hold the new spun-off company sell it regardless of price, which usually makes the best entry the one after the split, not before. Could this time be different? Sure. But I am not a forced buyer here, so I am happy to wait for what may be a better entry.

Final Thoughts

KBR has been on my watchlist for a while now, with dozens of hours of research behind it. It checks a lot of boxes, sitting right in the middle of several long-term tailwinds.

What has kept me out is the credibility lost by a management team that has been fantastic for over a decade, two complex businesses that are hard to forecast, and a spin-off that will likely open a better entry down the road.

Add it all up, and I see a good but not great opportunity right now. That is not good enough to beat what I already own. It is a high bar to interrupt compounding that I can’t confidently say KBR has.

If I get more confidence in their ability to grow the top line and margins, this could become a very compelling add. For now, I will be waiting and watching results.

Odds are I never buy it, but we will see how things play out.

Curious what I do own? Click here.

Full STS portfolio.

Ammonia (PURIFIER, KAAP, K-GreeN, H2ACT, Ammonia 10,000).

Hydrogen (H2KPlus, KRES). Olefins (SCORE alliance with ExxonMobil Chemical, K-COT). Refining (ROSE).

Phenol and specialty chemicals (phenol, bisphenol-A, polycarbonate, propylene oxide, NExOCTANE, acetic acid, vinyl acetate, PVC).

Plastics circularity (Hydro-PRT, exclusively licensed from UK-based Mura Technology, with KBR holding an 18.5% equity stake).

Energy transition advisory (sovereign hydrogen masterplans, carbon capture studies, direct lithium extraction with GeoLith SAS).

Reimbursable engineering and FEED services (Plaquemines LNG via the KZJV joint venture, Sonangol’s Lobito refinery, Saudi Aramco’s Petro Rabigh).

UK Nuclear / Frazer-Nash (Sizewell C, Rolls-Royce SMR, Sellafield decommissioning, KAD Nuclear JV). The Frazer-Nash UK nuclear practice formally moves from MTS to STS for fiscal 2026 as part of the cleanup ahead of the spin.

Allied defense spending detail. NATO Europe and Canada committed at the Hague Summit in June 2025 to 5% of GDP by 2035. The UK targets 3.5% by the same date. Australia’s 2026 National Defence Strategy raised its Integrated Investment Program to A$425 billion with A$887 billion in cumulative defense spending over the decade. The new spending is munitions, AUKUS submarines, integrated air and missile defense, cyber, autonomous systems, and supporting infrastructure. KBR’s UK and Australian government services franchises are built for that.

https://www.statista.com/statistics/1065865/ammonia-production-capacity-globally/

https://ammoniaenergy.org/wp-content/uploads/2026/02/AEA-LEAD-Plants-Executive-Summary-February-2026.pdf

Civil nuclear country targets through 2050.

U.S.: 4x nuclear generation.

UK: 4x.

Europe: 50% increase.

Canada: 2x or more from Ontario alone.

Global nuclear investment ran around $30 billion per year through the 2010s and could reach $100 billion per year to hit these targets.

Off 2025 segment revenue of about $2.2B for STS and $5.6B for MTS, 7% and 4% growth puts 2029 revenue near $2.9B and $6.5B, both below management's 2023 to 2027 bands of 11 to 15% for STS and 5 to 8% for MTS. At 17% and 11.5% segment EBITDA margins, segment EBITDA is about $493M and $748M, roughly $1.24B combined. Less about $130M of corporate, all-in adjusted EBITDA is about $1.11B, an 11.8% consolidated margin. Corporate is set at $130M to reflect the roughly $100M running today, plus the loss of shared overhead across two standalone companies and inflation, net of some optimization. In the sum-of-parts, that $130M capitalized at the blended 13.6x multiple removes about $1.8B.

STS comparables, EV/EBIT averages since 2020: Fluor ~15x, Johnson Matthey ~10x, Worley ~18x, KBR ~18x. Worley is the closest operating analog but lacks STS's licensed-technology portfolio.

Note I used EBIT here since Worley did not have EBITDA available in my software.

MTS comparables, EV/EBITDA averages since 2020: Booz Allen ~15x, CACI ~13x, Leidos ~12x. Anchored to the low end at 12x for slower growth and recent contract losses.

Bradie’s 2014-2024 track record. Backlog grew from ~$11 billion to over $23 billion. Trough-to-2025 revenue grew ~87% at an 8% CAGR through both organic growth and $3.5 billion of M&A. KBR’s peak gross margin pre-Bradie was 8.2%; he has delivered gross margins above that level, hitting new peaks each year, for nine consecutive years. He met or beat guidance for eight straight years before 2025 broke the streak.

For the purpose of a KBR shareholder assigning accountability for the TRANSCOM contract disaster, it’s the CEO’s, fully — bid through execution through disclosure. A CEO termination based on ethics and incompetence unlocks value here. While your EV/EBITDA multiples are a few notches above where I would feel comfortable underwriting a value investment, I also think the uplift from nuclear and oil and gas, as well as defense, will push revenue growth above the embedded assumptions.

Is your preference the spin off or the parent company or both?