Dassault Systèmes (DSY.PA) Notes

Dassault Systèmes is down 65%+ from its 2021 high, and most of the damage is recent. Down 40%+ in the past year, including its worst single day since 2002.

The market’s story is AI is coming for engineering software, and Bezos has raised $18B to do it.

Here’s the business the market is burying.

Their software builds working replicas of jets and cars inside a computer so companies can test them against real world physics before building a real world prototype.

Will the wing hold?

Will the passenger survive the crash?

Boeing and BMW bet billions on the answers before a single part gets made.

Through the entire decline, revenue, earnings, and free cash flow all grew.

And after all that, down 65%+ with a business still growing, it’s a pass. Because the price still isn’t low enough.

Welcome to 📉DeepValue Capital📈

I’m Kyler Johnson, a husband, dad, and self taught investor of 7 years.

24K+ subscribers and 259% returns from Jan 2024 to June 2026. I buy turnarounds and good companies at great prices.

Free Download")

How Dassault Makes Money

Dassault did €6.2B in revenue in 2025, serving 390,000+ customers across manufacturing, pharma, and retail. It started inside a French fighter jet maker in 1981 and has been selling virtual engineering for decades.

Three companies dominate engineering software globally, Dassault, Siemens, and Autodesk, and Dassault built the category.

What Customers Are Buying

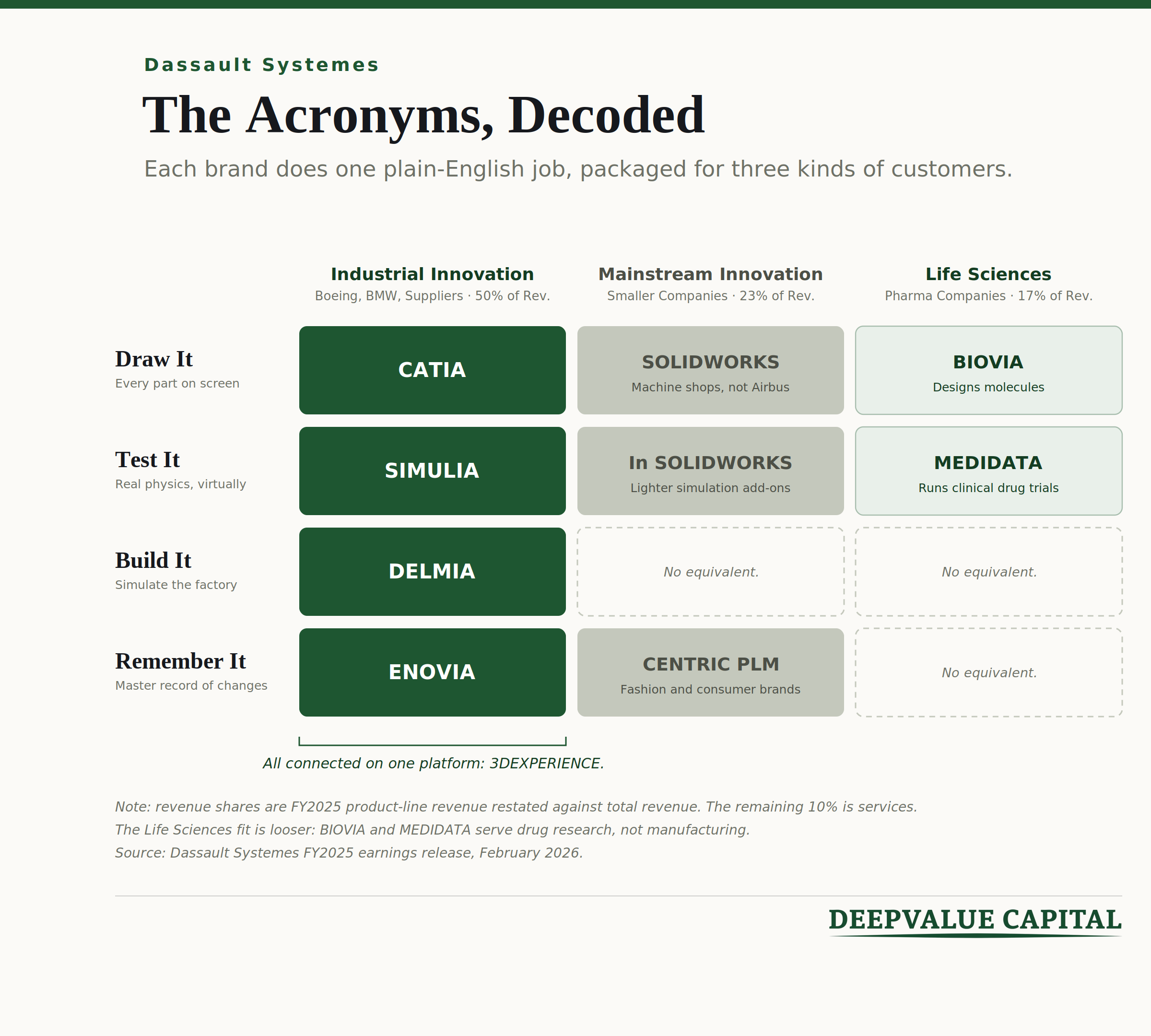

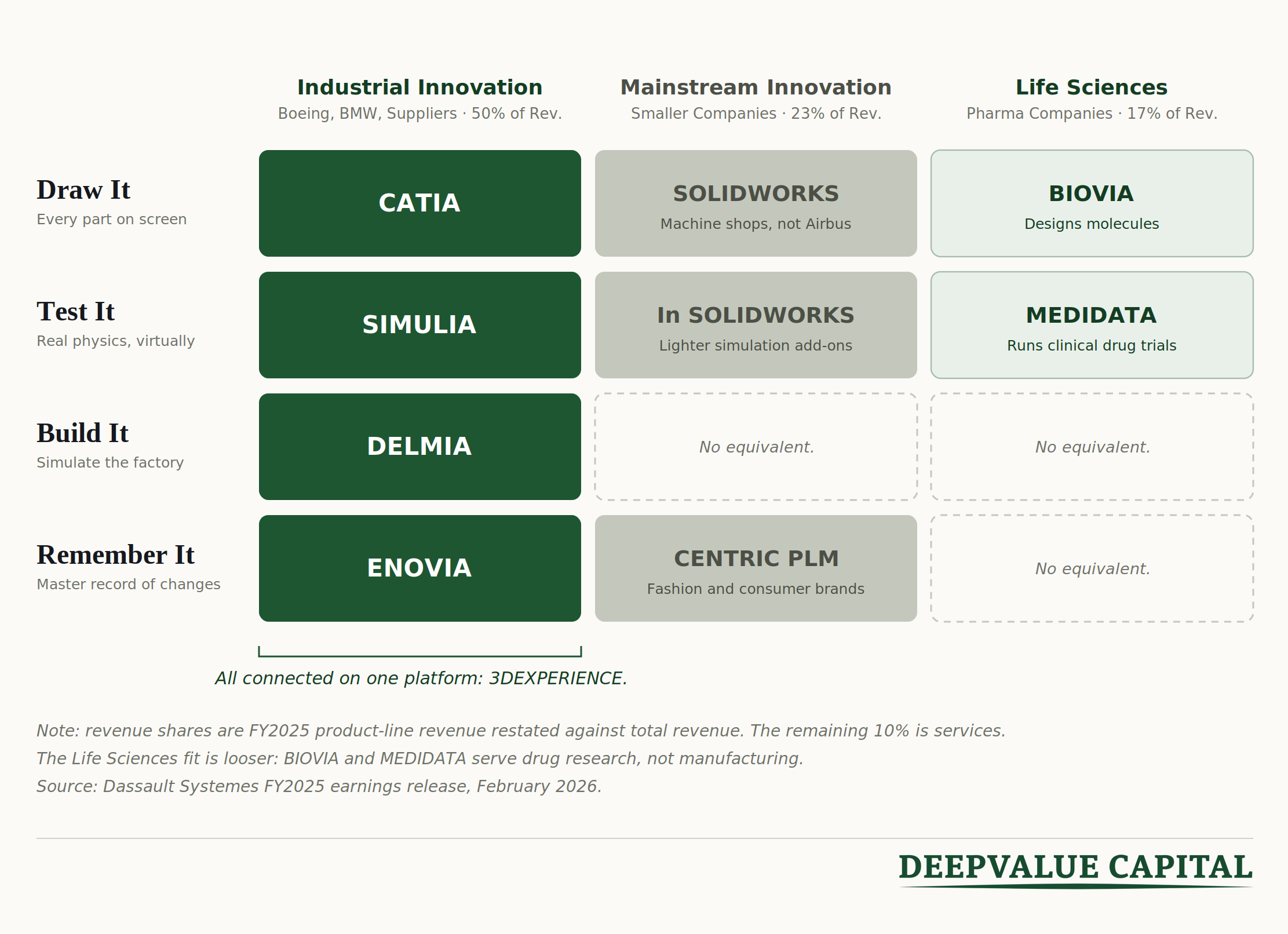

Dassault sells four things.

The brand names get confusing fast, so here’s the map. Everything they sell does one of four jobs, for one of three customer types.

Industrial Customers (~50% of revenue): The Boeings and BMWs and their suppliers, paying for the platform their entire engineering department runs on. When Airbus designs a jet, the engineers on that program work inside Dassault’s software, and so do the suppliers building its parts.

Mainstream Customers (~23% of revenue): They pay for lighter ready out-of-the-box versions, mostly SOLIDWORKS. The machine shop designing a bracket runs it the same way the giants run CATIA, at a tenth of the price.

Pharma Companies (~17% of revenue): They pay MEDIDATA to run the data behind clinical drug trials, the patient records and study results that decide whether a drug gets approved.

Services (~10% of revenue): The consultants who install the software and train the engineers.

Underneath all four, what customers are really buying is avoided cost. Every design flaw caught in software is a physical prototype that never gets built and a recall that never happens.

That’s why a company will pay thousands of dollars per engineer per year, decade after decade. The bill from Dassault is a rounding error next to what it prevents.

How They Charge Customers

Seats, ~74% of revenue. One engineer, one subscription, one year. A SOLIDWORKS seat runs a few thousand dollars annually, a high-end aerospace seat many times that, and large customers sign multi-year contracts covering hundreds of seats. Everyone pays upfront, so Dassault runs on its customers’ cash.

Old licenses, ~16% of revenue. A one-time license plus annual maintenance, and the most deferrable purchase a customer makes, which is why this line took the hardest hit in 2025 when auto budgets froze. Underneath the cycle it fades slowly anyway, since everything new Dassault sells, the cloud platform, Medidata, the AI layer, is subscription, so new money flows to the subscription line while this one lives off its installed base. This is the one true transition in the numbers, gradual and mostly by mix rather than by decree.

The new AI layer, <1% of revenue. Announced this February, read by the market as Dassault tearing up its pricing model, and a part of why the stock got repriced. What it actually is, and how the market got it wrong, matters enough that it gets its own section.

The Economics

The economics of all this are hard to beat.

Gross margins run 84%, because once the software exists, the next seat costs Dassault almost nothing to deliver. The one big real cost is building the software itself, with roughly 20% of revenue going into R&D every year.

And since customers pay upfront, the cash arrives before the work.

That combination, sticky software at 84% margins with a fifth of every sale funding next decade’s product, is the reason the stock has commanded a median 30x EV/FCF over the last 20 years.

Where New Customers Come From

Large manufacturers arrive through multi-year enterprise deals, and often they aren’t so much won as inherited. When Boeing runs CATIA, Boeing’s suppliers run CATIA.

Small manufacturers don't buy from Dassault directly. They buy from local resellers around the world, which handle the sale, the training, and the support in their own markets.

This funnel matters more than its size would suggest because customers grow through it. The startup that begins on a SOLIDWORKS seat becomes the mid-size manufacturer that buys the platform, so today’s small accounts are part of where tomorrow’s large ones form. That gets important later in this article.

Pharma companies arrive study by study. Every new drug trial needs a data platform, and MEDIDATA gets picked for more of them than anyone else.

Why Businesses Choose Dassault and Why They Stay

Companies choose Dassault because it has become the standard.

Its software has handled the largest, most complex machines in the world for four decades, regulators accept its test results because of the validation history behind them, and engineers still come out of school already trained on it.

When a company picks Dassault, it’s picking the proven certified path engineers were trained on.

Why they stay is even easier to explain. The software keeps getting more useful the longer a company runs it.

Every part ever designed, every test ever run, every certified version lives inside these systems, so each year of use makes the next year more valuable. Twenty years in, that history is one of the company’s most important assets, and it lives in Dassault’s software. Switching would mean walking away from it, retraining every engineer, and re-validating years of work, just to move to a tool that generally does the same job.

All that means renewal is the default, and it shows in the numbers. 82% of software revenue is recurring, €4.6B that arrives before a single new deal gets signed.

The best part is that staying put still generates growth, because a big piece of the growth comes from existing customers upgrading or growing. Thousands of companies still run Dassault’s older standalone tools, and Dassault is moving them onto the connected 3DEXPERIENCE platform, where design, testing, and records work together and the subscription costs more.

That platform revenue grew 10% in 2025, against 4% for the company overall, excluding currency. And the upgrade is still early. By Dassault’s own measure, only 41% of the revenue that could be on the platform is there today. The other 59% is the runway.

What Went Wrong

First, the shape of the fall.

The stock peaked in late 2021 at ~55x EV/FCF. 2022 cut that hard as rates rose, and then it traded flat from late 2022 until mid-2025. That's when growth estimates started taking real hits, and it has been sliding on weaker outlooks ever since.

Growth Slowed

Dassault's growth broke in 2024. The company grew 9% in 2022 and again in 2023, then 5% in 2024 and 4% in 2025, all excluding currency. February's guidance came in at 3 to 5% for 2026, the third step down in a row.

Three drivers sit under that slide.

Their biggest customers cut spending. Transportation & Mobility is Dassault’s largest industry vertical, and European automakers spent 2025 slashing engineering budgets.

Medidata broke. Pharma companies started fewer clinical trials for the second year running, and Medidata bills study by study, so fewer studies means less revenue, immediately. Life Sciences, a fifth of the company, fell 2% in 2025, its second consecutive decline.

The low end keeps leaking. Autodesk’s Fusion sells for roughly $700 a year against a few thousand for SOLIDWORKS, and it’s winning the newest, smallest shops. Dassault’s Mainstream segment grew 2% in 2025 while Autodesk’s manufacturing products grew 17%, and even after adjusting for an accounting change that flattered Autodesk’s number, the gap is wide.

Price is only half the attack, though. The other half comes from Onshape, which was built by the same people who created SOLIDWORKS in the first place. SOLIDWORKS is desktop software from the Windows era, where one engineer works on a file at a time and sharing means file servers and emailing versions around. Onshape runs in a browser like a Google Doc, with the whole team working in the same model at once. A five-person startup with no IT department doesn’t agonize over that choice.

Listen to how users complain about SOLIDWORKS and you’ll notice they almost never say it can’t do the work. They say it crashes before saves, that rebuilding broken models eats real hours, and that setting it up feels like software from a different era. Even the loyal base is uneasy. Each year’s list of new features keeps getting shorter, and longtime users openly ask whether Dassault’s development dollars have quietly moved to the platform.

The part that compounds is the pipeline. For twenty-five years, engineering students graduated fluent in SOLIDWORKS and asked for it at their first job, which is a big part of how it became the default. Now high school robotics teams and university programs are teaching Onshape and Fusion instead, because they’re free and run in a browser. That flywheel took decades to build, and it’s starting to spin for the other side.

None of this shows up as decline yet, and it may not for years. Decades of legacy files and engineers with ten thousand hours in the tool protect the installed base, which is why the leak reads as 2% growth instead of shrinkage. But the sentiment is running well ahead of the revenue, and the gap between those two is the thing to watch.

AI Became an Existential Question

Dassault charges per seat. One engineer, one subscription. The AI fear is aimed at the heart of that model, because an AI assistant doing engineering work doesn’t occupy a seat, and if AI makes each engineer twice as productive, customers need half the seats.

In early February, that fear went from concern to panic. Anthropic launched enterprise AI agents, and the selloff that followed erased $285B across software and adjacent sectors in a single session. One week later, Dassault’s soft guidance landed and the stock had its worst day since 2002, falling as much as 22%. In June it fell again when Jeff Bezos’s Prometheus, an AI startup targeting Dassault’s market raised another $12B.

Management’s response added its own uncertainty. Alongside the February results, Dassault announced new AI pricing tied to the value delivered, the layer teased earlier.

What the company meant was an addition on top of seats. The structure has three layers over the existing subscriptions. AI assistants and automation are priced in tokens, with management describing units of knowledge and units of work as “basically a token having a certain value” that customers can cap. And for the largest engagements there are outcome-based deals, where Dassault does the engineering work itself and prices the result, like a headlamp design automation priced at a share of the engineering cost savings. The layer exists so the work gets billed no matter who does it, human or AI.

And the outcome deals are less radical than they sound. A company running hundreds of seats was never paying list price, it negotiates a custom multi-year contract every renewal cycle. Outcome pricing changes what the number in that contract is indexed to, but not how the deal gets done or who’s sitting at the table.

But that’s not the framing management led with. On the February call, their own words were that Dassault was “evolving beyond seat-based pricing toward value-based models.” The CEO was out telling press “my dream is to price the object, which has been generated automatically, based on the value.” When that’s the language, you can see what investors heard. The CFO spent the Q&A walking it back, explaining that the AI companion still needs CATIA, that it’s the one using CATIA, not substituting it. It didn’t stick.

The plainest version, that the new products “are not replacing the existing one” and the portfolio “will stay,” didn’t come until the April call, two months after the damage was done. What the market heard in between was the seat model ending. Announcing a pricing change mid-crisis, vaguely enough that investors heard replacement, turned a product launch into a forecasting problem, and markets pay less for what they can’t forecast. They also began publishing a new metric, annual recurring revenue, so investors could track the business through the shift. Companies don’t hand you new metrics when the old ones look good.

Is the Slowdown Cyclical or Permanent?

Truthfully, it is both.

Auto is cyclical, with one structural catch. Volkswagen is cutting more than 35,000 German jobs by 2030. BMW just cut its 2026 margin guidance from 4-6% to 1-3%. When your biggest customers are doing that, they postpone or downsize software deals.

Here’s the tell that this is customer health and not lost accounts. In the fourth quarter of 2025, Europe fell 5%, dragged down by French and German auto weakness. One quarter later, Transportation & Mobility was one of the main contributors to Dassault’s growth, led by the Americas. The demand came back through different customers on a different continent. Engineering seats follow whoever is doing the engineering.

What protects Dassault is that nearly everyone doing that engineering is already a customer. Volkswagen runs vehicle development on the 3DEXPERIENCE platform. BMW is building its next engineering platform on it. Volvo Cars, owned by China’s Geely, develops its EVs on it. JLR just extended it across every vehicle program worldwide. NIO designs on it, and Tesla has run on CATIA for years.

That’s the shape of the whole industry, and it means a European automaker losing a sale doesn’t destroy a seat. The engineering behind the winning car is usually running on the same two companies’ software, and often on Dassault’s. Share shifts between automakers mostly reshuffle seats inside the same duopoly.

I won’t pretend Europe itself bounces back soon. Bain finds German OEMs planning to cut R&D intensity by an average of 35% by 2027, because Chinese competitors develop vehicles at roughly a quarter of their cost. What I will say is that the engineering happens somewhere, and wherever it happens, Dassault is usually underneath it.

Medidata is already turning. Clinical trial software lags the biotech funding cycle by several quarters, and the funding cycle has turned. Biotech venture funding jumped 71% quarter over quarter in late 2025, and the big trial-running companies are reporting record backlogs. Medidata was still down 3% in Q1 because it's living off weak 2025 bookings, and management said as much, calling it a carryover while noting that new bookings in the quarter were already trending positive. The same lag means the reported numbers can stay ugly into early 2027 even if the recovery is real.

The thing that would change my mind is Veeva. If Medidata is still shrinking in late 2026 while trial activity recovers, that tells me Veeva is taking share, and I'd have to reassess Dassault’s future.

The low end has issues. Autodesk’s Fusion at $700 a year keeps winning the newest, smallest shops. Dassault keeps the professional core, since Fusion still struggles with large complex assemblies, but the bottom of the funnel is leaking, and that’s where future customers form. Mainstream did bounce 14% in the first quarter, mostly Centric recovering, but the leak was never a one-quarter story. New shops keep choosing Fusion first, and that caps how fast this segment can ever grow, and potentially the company's long-term runway with it.

And one piece is quietly working in their favor. Europe is rearming, Airbus is sitting on years of backlog, and aerospace and defense is Dassault’s deepest home turf. In April 2025, Airbus extended its partnership across all civil and military aircraft programs, which also answers the boring competitive question. The real enterprise fight is a two-horse race with Siemens, and the biggest account on the board just re-upped.

Add it up and the recurring floor grows mid single digits on its own. Auto and Medidata improving add a point or two through 2028, defense adds on top, the leak takes a point off, and the old license line, flat this year and fading slowly as new offers go subscription, gives back maybe half a point over the horizon.

Then there’s the new AI layer. €50M of backlog in six months is a €100M annual pace from a product line that didn’t exist a year ago, sold into 390,000 accounts Dassault already bills. I give it one point of growth, and whether it deserves more gets answered at November’s Capital Markets Day.

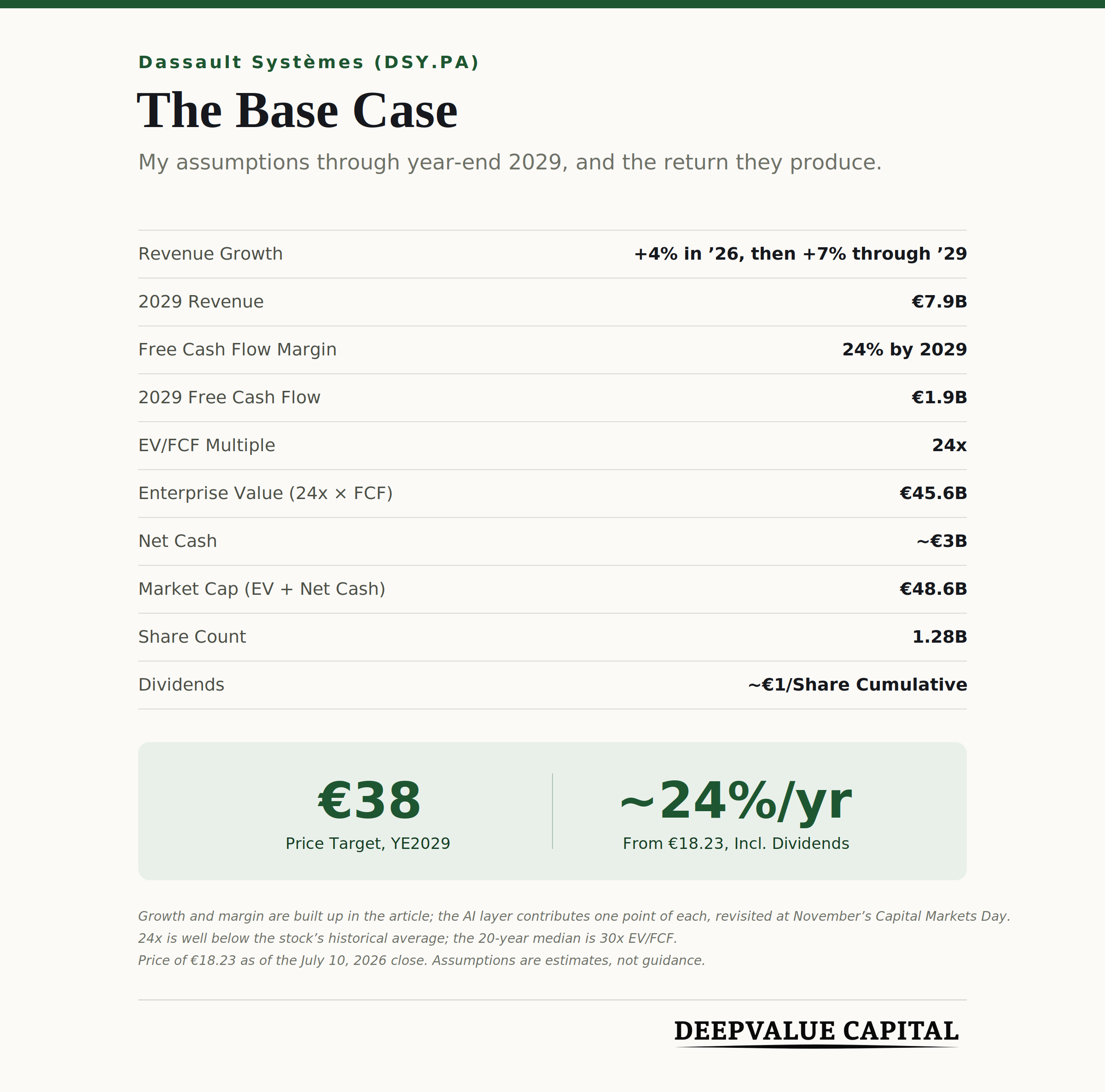

So for my numbers, 4% growth this year while the cycle bottoms, then 7% a year through 2029 as it recovers. That lands 2029 revenue around €7.9B.

One note on those numbers. Management’s target is still higher than mine. They’ve promised to double EPS to €2.20-2.40 by 2029, a target already delayed once, with the old revenue promise quietly dropped from under it.

On margins, they deserve real credit. Headcount is falling, they’re using AI to cut their own costs, executive pay is tied to cash conversion, and they’ve expanded margins through this whole slowdown, guiding another 0.2 to 0.6 points higher for 2026 in a year they only expect 3 to 5% growth. Run that pace forward and it carries a point by 2029.

The AI layer carries a second point, and the math here is worth a moment. AI credits are worse business than seats, because every AI task burns computing power that Dassault pays for, while a seat costs nothing to serve. But credits don’t add salespeople or R&D, the costs that eat most of every seat euro. So a credit euro converts to more free cash flow than the company’s average euro does today, and the mix pulls the whole margin up even while gross margins drift down. The offset is timing, since customers pay for seats up front, and outcome deals could push that cash later.

Weighing all of it, I’m using a 24% free cash flow margin by 2029, two points above the seven-year record.

Can the Moat Survive AI?

The moat has three layers, and AI is only really fighting one of them.

The drawing layer is contested. Text-to-CAD tools exist and they work, for simple parts. Independent testing found they handle brackets and gears, then fall apart on anything complex.

Bezos’s Prometheus has raised $18B with about 150 employees and no product. And the AI connectors Anthropic built work inside Autodesk Fusion, which tells you where this fight is actually happening. It's at the low end, inside the competitor's cheaper tool, aimed at SOLIDWORKS. It’s real, and it’s contained to the SOLIDWORKS line, roughly €1B by my estimate, about a sixth of software revenue.

The testing layer holds. When SIMULIA says a wing survives its load, regulators accept the answer because of decades of validation behind it. An AI’s best guess about physics isn’t certifiable. In engineering, a hallucination is a structural failure. Even Dassault’s own AI push with NVIDIA builds on top of validated physics, because there’s no substitute underneath.

The memory layer is the strongest, and it’s the one the market has read backwards. This is the master record of every part, test, and certified version across an aircraft program that runs 20 years. AI can sketch you a bracket. It can’t be the legally authoritative answer to which of 40,000 parts is the certified one.

But holding customers in is only half of what the record does. It’s also what makes Dassault’s own AI worth paying for. An assistant automating design work is only as useful as what it knows about the products it’s working on, and the design history it needs sits in Dassault’s systems and nowhere else. Dassault’s AI can read 20 years of a customer’s decisions. Siemens’ can’t, and neither can anything Bezos builds, because the data they would need to train on doesn’t exist outside Dassault’s walls. Prometheus itself acknowledges there is no internet of manufacturing data to ingest. It has to be built from scratch, and the closest thing to it already sits in Dassault’s record.

The moat and the new pricing model are really one bet. Dassault can price AI work against the value it creates only because no competitor can create the same value on that account, and the record is the reason they can’t.

And the moat shows up in the numbers, which is the only place a moat counts. Gross margins have sat between 83% and 84% for seven straight years, through a pandemic, an acquisition, and this slowdown.

Recurring revenue grew 6% in the company’s worst year. Returns on capital have climbed every year since 2020, from 11% to 15%, which is not what full disruption looks like.

The question that decides this is whether Dassault gets paid for what AI creates, and the new pricing layer is where that gets settled. Adobe and Autodesk are the reference points here, both survived tearing up their pricing, and both spent two to three ugly years doing it. Dassault’s road should be smoother than that. The genuinely painful change, licenses becoming subscriptions, is mostly behind it at 74% of revenue, and the AI layer gets added on top of contracts the biggest customers already renegotiate every renewal cycle, so nothing is actually being torn up.

So I think they defend their pricing power, and the early backlog has earned the layer a modest place in my numbers. One point of growth, nothing more, and I pay for what's proven and let the rest be upside. That thinking sets the multiple. This stock traded at 30x+ EV/FCF from 2016 through 2024, and in the 20s for years before that. A proven, moaty business growing 7% deserves something in the low-to-mid 20s, so I'm using 24x.

Can We Trust Management?

Split the question in two, because the record splits in two.

On profits, yes. EPS has landed on target every year. Margins ticked up in 2025 even while revenue missed. They generate €1.6B of operating cash flow, bought back €340M of stock, paid €343M in dividends, sit on €1.5B of net cash, and the share count has drifted down five years running. No dilution, no empire building.

On growth, no. 2024 guidance started at 8 to 10% and got cut. 2025 started at 6 to 8% and got cut. Two years, two cuts, and the 3 to 5% bar for 2026 is the first one set low enough to beat. Daloz has admitted as much, saying he’s done chasing top-line guidance quarter after quarter.

The pay structure explains the whole pattern, and there’s no guessing needed, the criteria are published. The CEO’s stock awards vest on three things. The financial piece is 80% of the award, split two thirds on EPS growth and one third on cash conversion, which just measures how much of reported profit turns into cash. The last 20% is an ESG scorecard. Revenue appears nowhere in that list. So when revenue disappoints, nothing in his paycheck breaks. They flex costs, deliver the EPS number he’s paid on, and the growth guidance takes the hit. The incentive is working exactly as written. The profit guidance is the part to trust, and the growth story is the part to discount until they prove it.

His pay is built almost entirely on those targets too, roughly €13M a year with over 90% of it variable, and he owns about €54M of stock, per outside estimates. His own wealth rides on hitting the EPS targets, and guiding revenue high does nothing for his paycheck.

Then there’s the departure. Bernard Charlès spent four decades building this company, and he left the board ten days after the worst day in its stock history, effective immediately, for personal reasons. The succession itself was the prepared part. Daloz is a 25-year insider who ran finance, then operations, and had already been CEO for two years, with the Medidata acquisition as his deal. The exit didn't look prepared. Orderly chairman transitions get announced months ahead, and same-day resignations don't happen when everything is fine. Daloz now holds both jobs, which is normal for a French company. The part that changed is that the founder who used to look over his shoulder is gone.

My verdict is a disciplined operating team with a two-year habit of overpromising growth, now running a plan they’ve finally sized to hit. That’s good enough to keep going, and not good enough to pay up for.

What Is This Company Worth?

So where does this leave us. A real moat in its two deepest layers. A trough that’s probably this year. Management you can trust on profits. And a stock at 13x EV/FCF that traded at 55x.

That sounds like a buy. Then you run the numbers.

I grow 2025 revenue 4% this year while the cycle bottoms, then 7% a year through 2029. That’s €7.9B of revenue. At the 24% free cash flow margin built a few sections back, one point from cost discipline they’re already delivering and one from the AI layer, they earn €1.9B of free cash flow. I put 24x on it, below anything the stock has traded at in its public life.

The cash matters too. They’ll generate over €6B of free cash flow between now and 2029, and it has to go somewhere. The dividend keeps growing, they raised it weeks after the crash. Buybacks step up like they did in 2022, the last time the stock got cheap, and the share count shrinks to 1.28B. Maybe a deal or two. They still end 2029 holding around €3B of net cash.

That gets me to about €38 per share by year-end 2029, plus close to a euro in dividends along the way. From €18.23, the 7/10/26 close, that’s better than a 2x. About 24% a year.

24% a year on a business this durable is a clear buy for most portfolios.

My hurdle is 30%, and this doesn’t clear it.

The assumed 7% growth builds in macro improvements and the AI layer helping. The 24% margin already builds in expansion that's likely but not guaranteed. For the math to get interesting, the stock needs to be near €15.50, and even then it just qualifies for a deep dive. Not an instant buy.

My Thoughts

This is a very solid business and I’m not buying it.

The market is pricing Dassault like traditional software, the kind AI is supposed to eat. I don’t think that’s what this is. The Boeings and BMWs of the world design the most complex machines on earth inside these systems, and 20 years of their parts, tests, and certified decisions live there and nowhere else.

That history is exactly the data an AI challenger would need to train on, and it doesn’t exist outside Dassault’s walls. Bezos raised $18B to build the disruptor, and so far there are about 150 employees, no product, and an open admission that the training data has to be created from scratch.

They do have real issues, especially at the low end against Autodesk, but real issues are a long way from destroying a company with this kind of customer lock-in.

Price and value are two different things. In 2021 the market set the price, 55x free cash flow, and it has spent the four years since trying to figure out the value, with AI shifting the landscape underneath the whole search. That kind of answer takes time, and it usually overshoots on the way down.

That is where I search for opportunities.

For the math to get interesting, the stock needs to be near €15.50. Until something changes, Dassault sits on the watchlist at €15, and that's where I'd pick this file back up.

You just read a full breakdown of a new idea, free, with nothing held back. This is the standard behind everything I publish. What members get is the portfolio itself, the names I actually own with full deep dives, the buy and sell calls, and updates as each thesis plays out.

If that's the kind of work you want in your inbox, that's what a paid membership is.

To read my full disclaimer click here.

An incredible name! Really hoping for some management changes though that seems unlikely. Communication with investors has been very poor

Very interesting, I had $AM on my radar, specifically because of the business aviation growth and the need for military applications. Your article is very in-depth. I don't believe the AI component will shatter revenues continually, though their biotech probably will pull back as you say.