Methode Electronic | First Look: Buy or Bail?

If you are looking for undervalued stocks this article is designed for quick idea generation. Is Methode Electronics a good buy right now?

MEI 0.00%↑ is looking interesting today for several reasons. Stick around as I cover everything I find in my first look.

An 85% plunge creates a potential value play in automotive and industrial technologies.

From switches to sensors, this diversified manufacturer trades at 4x normalized free cash flow.

A new CEO steps in as the company pivots, with manufacturing trends setting the stage for a comeback.

Let's be real, investing can be hard. Constant bad news, the latest hype stock going to the moon, tons of potential strategies, and it take huge amounts of time.

Let me help you shortcut that process.

Become a paid subscriber and on top of getting consistent quality idea generation you get curated deep dives, company updates, and exclusive portfolio access. What are you waiting for?

Here are some other articles you will love!

Ticker: MEI

Market Cap:$240.91M

Stock Price:$6.75

Before we can look deeper at why any company is interesting you need to first know what they do. After all no matter how good they look, if they aren’t in your circle of competence, stay away.

In their fiscal year 2024 Methode broke their business into the following segments:

Automotive (53.7%): Switches, sensors, lighting, consoles, and others.

Industrial (41.3%): Lighting, remote controls, braided cables, custom products and many others.

Interface (4.8%): Cooper transceiver, distribution units, and consumer touch panels.

Medical (0.2%): Shut Down October 2023

And they operate manufacturing plants out of several countries including the US, Mexico, Malta, Belgium, China, and Egypt.

Methode caught my eye in mid 2024 in the middle of their steepest drawdown but at the time I felt it was not cheap enough.

Now there are a few reasons why I think they look interesting after their plunge.

Down 85%+ from highs.

Median ROIC since 1991 of 13%.

Current $250M market cap on a normalized FCF of $63M, or about 4x FCF. (Based on the TTM $1.07B in Rev and average FCF margin of 5.88%)

Historical median FCF multiple of 16x.

New CEO and leadership.

Manufacturing and industrials are beaten down but global manufacturing is turning up.

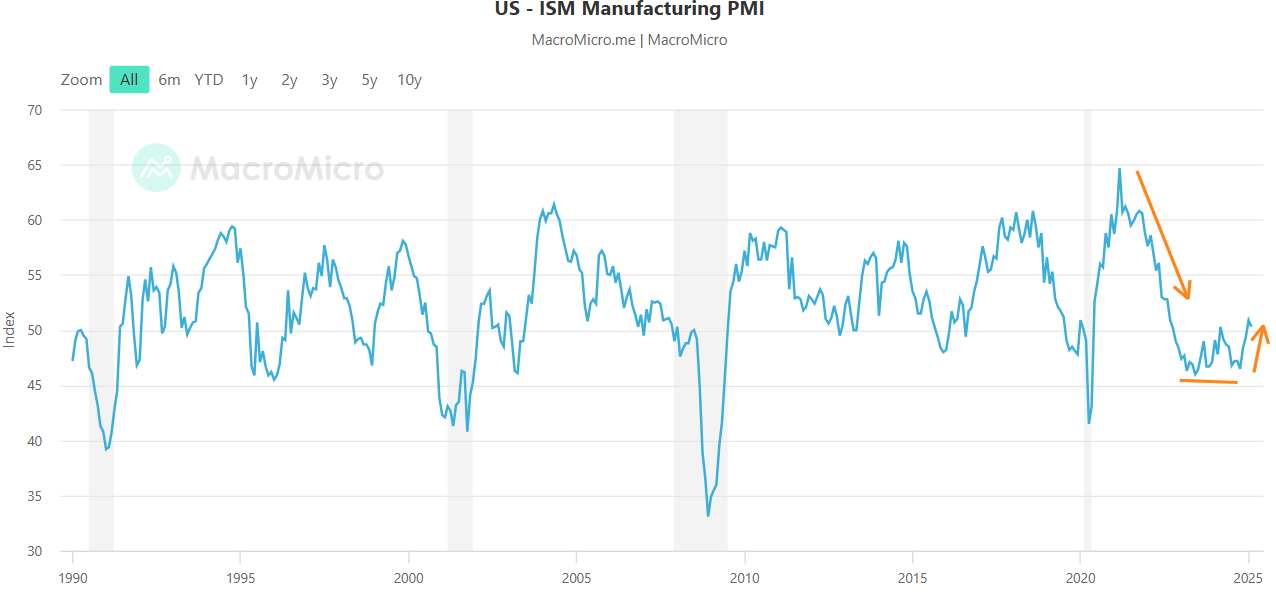

Lets me elaboration on the manufacturing sector. After Covid manufacturing boomed, Catching up to demand but soon lost steam. Then in 2022 started to contract. A contraction in manufacturing is defined as the ISM PMI falling below 50.

It remained below 50 until 2025 meaning manufacturing has been in a recession for over 2 years. Things are now turning back up which will be a tailwind for all manufacturing companies.

Even with manufacturing truing back up there is work to do before I would consider taking a position. In any turnaround the most important question is on their leadership.

Does the CEO have a track record of success(es) with that give you confidence they will execute on the turnaround?

Other questions are important but secondary to the one above.

What are the full details of their business turnaround?

What catalysts will drive the turnaround outside of the internal changes made?

Are management incentives aligned with shareholders?

What major risks are there that would cause the future to be materially different?

If you can get clear on these questions and the company still looks interesting after it could be a solid opportunity.

If Methode returns to their average FCF margin and multiple on their current revenue you would see a 4x return. This would likely take around 3 years which would get you almost a 60% CAGR! If it took 5 years that is still a 32% CAGR which is pretty solid.

Opinion

Methode’s new CEO John DeGaynor previously ran Stoneride from 2015-2023. And before that was a VP at SRG Global.

In my research I would describe him as an ok CEO. In his 8 years at Stoneridge he delivered about 150% returns for shareholders. Which isn’t bad but isn’t the world class I look for. When he left the company abruptly in 2023 the previous few years had been a continued margin slide.

Cooper Standards’ margins bottomed in 2022 and unlike Stoneridge their margins fell due to a drop in revenue. Stoneridge saw costs increase which ate up margins.

It is for that reason of questionable management I favor Cooper Standard as a play on manufacturing and automotive. But if CPS is not for you or you want a little more diversified play Methode is worth some work!

Disclaimer:

This content is provided for informational and entertainment purposes only and should not be construed as professional financial or investment advice. The opinions expressed herein are solely those of the author, based on personal research and analysis, and do not reflect the views or advice of any financial institutions or licensed professionals. I do not have access to your personal financial situation, goals, risk tolerance, or investment preferences, and therefore cannot provide personalized investment recommendations. It is essential that you conduct your own research, carefully consider all relevant factors, and consult with a licensed financial advisor or other professional before making any investment decisions. Investing inherently involves risk, including the potential loss of principal, and past performance is not indicative of future results. I am not responsible for any decisions, actions, or outcomes resulting from the use of this content. Always ensure that your investments align with your personal financial situation and long-term objectives.

See you in the next edition!