Comstock Resources (CRK) Deep Dive

Welcome to 📉DeepValue Capital📈

Credit for this idea goes to Thomas J. Hayes.

Comstock Resources is probably not a company you have heard of. They don’t do anything flashy, they are a natural gas producer.

And they do it at costs 40%+ lower than peer average on some of the most resource rich land in the country that just so happens to be right in the heart of data center and LNG demand.

So yes, they might not be flashy, but the opportunity they present sure is.

The Company

Headquartered in Frisco TX, Comstock controls 806,980 net acres across East Texas and Louisiana.

Production runs ~1.2 Bcf/day (billion cubic feet per day) of dry gas, meaning no oil or natural gas liquids byproduct. They are a pure play on natural gas.

Part of what makes them low cost is that they built their own gathering and processing system through a subsidiary called Pinnacle Gas Services.1 That pipeline is now scaling toward 2 Bcf/day of capacity giving them room to grow.

And they have room to grow. Based on current production and my conservative estimates they have ~30 years of inventory (66 Tcf) before they run out. And that's only the inventory economic at $5/Mcf. Roughly two thirds more sits locked behind higher gas prices or better technology.

If that unlocks, the runway is much longer.

So if everything looks great, what is going on today?

What Broke

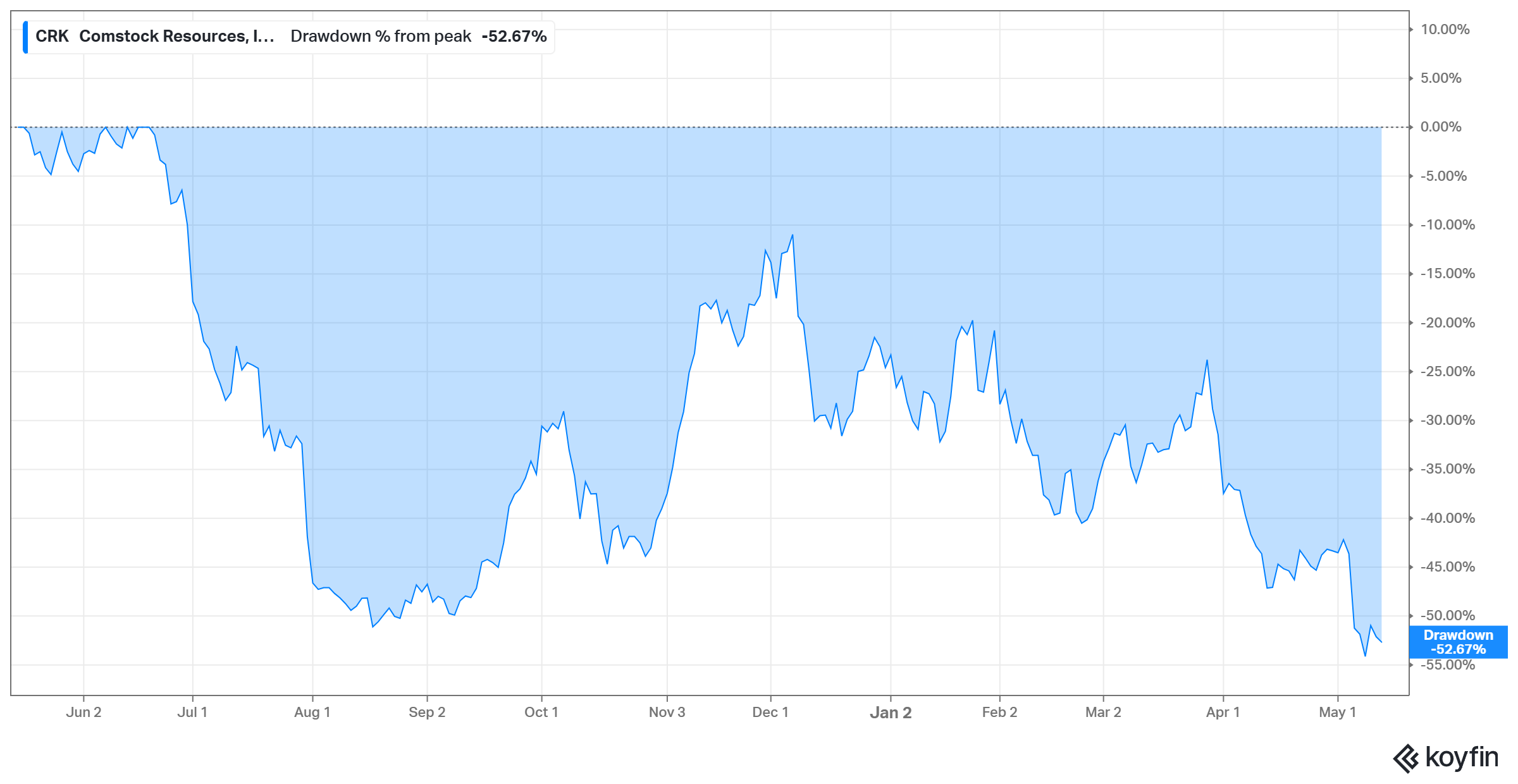

Pure play gas means Comstock's stock moves with gas prices. Both have been soft. Henry Hub trades at $2.84/MMBtu today, ~19% below the 2025 average of $3.52. CRK is down ~53%.

I bought CRK in early 2024 when gas was worse. Three things had hit at once:

Warmest U.S. winter on record.

Record high production.

No new LNG export capacity coming online (a Freeport train was even out on a January Arctic freeze).

These pressures led to storage ballooning to 39% above the five year average, forcing prices down.

Today is a milder version of 2024.

Record production.

Unusually mild winter and warm spring.

Storage now sits about 7% above the five year average. Less extreme than 2024, but the pressure is the same.

The good news is none of this is permanent damage. Demand is coming. LNG capacity is ramping. Gas fired data centers are coming online.

Management has to navigate the gap. Costs, capex, growth, and debt.

To read my full disclaimer click here.

Can We Trust Management?

Jay Allison and his team have run Comstock for over thirty years. The proof of that experience shows up in one very important number.

Production cost.