A Forgotten Giant Quietly Restructuring | First Look

Leggett & Platt is down 90%. Here's what's changing, what's at risk, and what could unlock 5x upside. (I do not own LEG)

Hey All 👋

Welcome to 📉 DeepValue Capital 📈

New here? Check the two links below.

How I find companies to invest in.

Now to todays article!

How do once-great companies end up down 90%… and can they ever bounce back?

This week I’m looking at Leggett & Platt (LEG)—a $6.85 stock the market has written off.

It’s easy to see why:

Revenue has declined for years

Margins have eroded

And the once-reliable dividend was just eliminated

But look under the surface, and there’s an interesting shift starting to play out…

Management is cutting ~$65M in structural costs

Selling off non-core businesses

Freeing up $220M/year in cash from the dividend

And aggressively paying down debt

Is it enough to matter? That’s what I’m trying to figure out.

This post will walk you through:

✅ What Leggett & Platt does

✅ Why the stock has collapsed

✅ What management is changing

✅ Key risks and upside math

✅ And what might make this worth tracking long-term

3 More Articles You’ll Love:

Investors often miss long-term gains by focusing on short-term noise.

My strategy of targeting turnaround deep value companies has led to market-beating returns this year—and can help you do the same. (Hint: Paid subscribers get access to the best content like portfolio access, trade alerts, and deep dives.)

🛏️ What Does LEG Even Do?

Leggett & Platt is a 140-year-old manufacturer of physical products you interact with every day but never think about.

Their business is split into three core segments:

Bedding Components

Innersprings, foundations, adjustable beds

They supply the guts behind most mattress brands

Furniture, Flooring & Textile Products

Recliner mechanisms, flooring underlay, carpet pad

Sold to home goods retailers, flooring manufacturers, and furniture OEMs

Automotive & Specialized Products

Suspension systems, seating components

Largely sold into car OEMs and commercial transport

They’re also vertically integrated in steel, giving them some raw material cost control across segments.

Until recently, they had an Aerospace unit. But it’s being sold off in 2025 to focus the business and pay down debt.

🔻 What Went Wrong?

Let this be a lesson in slow-motion decay:

1. Leverage Creep

In 2019, LEG acquired ECS (a foam mattress supplier). It added debt to fund the deal, nudging leverage higher. But it still looked ok at the time.

2. Margins Collapsed

Gross margins peaked at 21.85% in Q2 2021. Today? Just 17.4%.

That’s a 450bps drop, which matters even more when you're carrying debt.

3. Dividend Stayed On Too Long

Even as demand fell and margins shrank, LEG kept paying its dividend, $220M+ per year. Management likely assumed the softness was temporary.

It wasn’t.

4. Demand Fell Off a Cliff

Bedding: Down 28% since 2021

Furniture/Flooring/Textile: Down 16.7% since 2022

Automotive: Fell just 5% from 2023, their most stable segment

With margins down, debt up, and demand shrinking things spiraled into the 4.75x Net Debt to EBITDA range.

🧱 The Restructuring Plan

Management is now doing what they should’ve done earlier:

🔧 Structural Cost Cuts

Targeting $60M–$70M in permanent SG&A and operational efficiencies

Facility consolidation, headcount reduction, footprint optimization

💸 Cash Reallocation

Eliminated most of the dividend → Frees up $220M/year

Proceeds from Aerospace divestiture in 2025: ~$240M after tax

Targeting $60M–$80M in real estate sales through 2026

In 2024, they already paid down $126M in debt. That trend should accelerate in 2025 and beyond.

📈 Are Management Incentives Aligned?

One of the most important questions in any turnaround: Is management playing the same game as us?

At Leggett & Platt, the answer is: Mostly yes.

CEO Karl Glassman owns ~0.9% of shares outstanding, which may sound light—but represents a significant portion of his personal net worth. That makes his alignment real, even if not massive in percentage terms.

His 2024 compensation is also tied to the right things:

88% of total pay is variable

Annual cash bonus: 65% based on EBITDA, 35% based on cash flow

Long-term equity awards:

Tied to total EBITDA

ROIC

Adjusted by Total Shareholder Return (TSR) vs a large peer group

🔍 TSR is just a fancy way to measure:

Stock price + dividends over time, divided by where it started.

It shows real investor return, not just accounting profit.

✅ This setup heavily rewards profitability, cash generation, ROIC, and debt reduction. Which is exactly what shareholders should want right now.

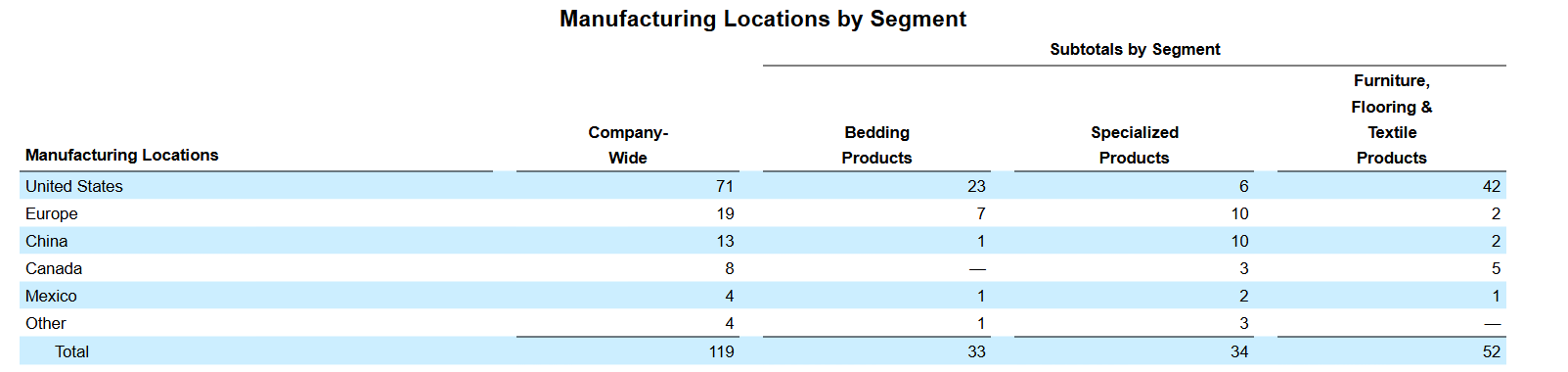

🌍 What About Tariffs?

Good news here: LEG is relatively insulated from the current tariff narrative.

They operate 119 plants in 18 countries—but 71 of those are in the U.S.

Most manufacturing is in the region it serves, and their vertical integration in steel lowers outside supplier risk.

Bedding? Mostly U.S.

Furniture & flooring? Mostly U.S.

Automotive? More global, but diversified

Bottom line: tariffs will impact the company, just not as much is you may expect. Especially compared to peers relying on heavy China exposure.

🔮 The Hidden Tailwind

Let’s zoom out for a second…

Who buys mattresses, furniture, and flooring?

People in their 30s to mid-40s, starting families, buying homes, moving up the spending curve.

Right now, the Millennial generation (largest in U.S. history) is entering their peak housing spend years.

That alone could boost LEG’s bedding and furniture segments over the next 3–5 years without them doing much of anything.

If management does execute? That tailwind gets a multiplier effect.

⚠️ Risks I'm Watching

Execution risk is high. If cost cuts run over or take too long, liquidity tightens.

Leverage is still elevated even after recent paydown.

Demand softness could persist longer than management expects.

Competition pressuring margins and market share making the pain structural not just short term.

This is the huge piece of work I did NOT perform for this company. In any deep dive before you buy a company you must understand their competitive position. This article is only a first look.

✏️ Back-of-the-Napkin Valuation

Let’s keep this grounded.

Management expects 2025 revenue of $4B–$4.3B, but that’s before subtracting $190M lost from the Aerospace divestiture and another $80M from business restructuring. Adjust for both, and you get a true post-divestiture range of $3.73B to $4.03B.

Let’s split the difference:

Midpoint = $3.88B

Historically, LEG has earned a 9% free cash flow margin, which implies:

$3.88B × 9% = ~$349M in potential FCF

Their historical FCF multiple is ~13.4x—but let’s stay conservative with 12x:

$349M × 12 = ~$4.19B valuation

That’s nearly 5x upside from today’s $885M market cap if management executes, margins rebound, and debt comes down.

There are real risks but at this price, the math does not require perfection.

Disclaimer:

This content is provided for informational and entertainment purposes only and should not be construed as professional financial or investment advice. The opinions expressed herein are solely those of the author, based on personal research and analysis, and do not reflect the views or advice of any financial institutions or licensed professionals. I do not have access to your personal financial situation, goals, risk tolerance, or investment preferences, and therefore cannot provide personalized investment recommendations. It is essential that you conduct your own research, carefully consider all relevant factors, and consult with a licensed financial advisor or other professional before making any investment decisions. Investing inherently involves risk, including the potential loss of principal, and past performance is not indicative of future results. I am not responsible for any decisions, actions, or outcomes resulting from the use of this content. Always ensure that your investments align with your personal financial situation and long-term objectives.

See you in the next edition!

Fascinating breakdown—this is one of the few recent posts that actually honors the structural tension between short-term impairment signals and long-cycle constraint reconfiguration. I’ve been modeling LEG through a velocity-based asymmetry lens (essentially looking at where internal constraint realignment could outpace market skepticism), and your analysis aligns with the early-stage indicators I’m watching for. If management executes even half of what’s outlined, the feedback loop between deleveraging and valuation multiple normalization could trigger more upside than the broader market seems prepared to price in right now. Appreciate the rigor here—subscribed.